Voya’s second edition of our biennial defined contribution (DC) plan participant survey seeks to better understand participant sentiments about financial and retirement planning priorities, the challenges and concerns participants face, and the services they may need—informing how DC plan sponsors and DC specialists can build more robust and competitive employee benefits programs.

About the survey

Welcome to the second edition of Voya Investment Management’s survey of retirement plan participants. The survey seeks to better understand participant sentiments about financial and retirement planning priorities, the challenges and concerns participants face, and the services they may need —informing how defined contribution (DC) plan sponsors and DC specialists can build more robust and competitive employee benefits programs.

Economic backdrop

We conducted our survey on January 23 and 24, 2025, a few days after the presidential inauguration.

As participants were completing the survey, the U.S. appeared to be emerging from the pandemic’s long-tailed aftershocks stronger than before. The cloud of inflation hanging over markets had slowly started to dissipate, unemployment was below historical norms, and markets had embraced the pro-growth prospects of deregulation and tax cuts.

Key findings

- Participant retirement preparedness sentiment increased significantly in 2025, with 69% indicating they feel very or somewhat prepared for retirement. Still, many participants would benefit from additional support from plan sponsors and DC specialists, as more than half of participants expressed concerns about inflation, market volatility, and the economy.

- Many participants did not view themselves as experienced investors, and the past few years have had mixed impact on their confidence. This suggests that many would welcome reassurance and support on key topics, such as the potential benefits of their plans and support for important decisions.

- Many participants reported relatively low levels of confidence in making key retirement-related decisions, particularly for decisions relating to retirement income and transition services, suggesting demand for additional support.

- Participants indicated strong interest in education related to retirement income and investment decision-making. Other areas where participants would welcome guidance included managed accounts, auto features, retirement drawdown strategies, and financial wellness topics. Promoting these services can help drive better outcomes for participants (and sponsors). Many of these products/services help address areas in which participants cited low levels of confidence.

- Many participants haven’t decided on their retirement date (especially those over age 50), possibly due to decreased confidence in meeting their retirement goals given high inflation and concerns about insufficient savings. About one-third of participants said they aren’t sure about their plans for their retirement assets after they retire.

- Participants generally viewed their employers as a trusted source and value their employer-sponsored retirement plan (ESRP). There is an opportunity for employers/sponsors to retain employees by offering services/support in some key areas, including improving overall financial wellness, support for key decisions, and retirement income planning.

- 15% of participants self-identified as a caregiver, and 5% reported having a disability or special needs. Two-thirds said they are very or somewhat interested in comprehensive planning resources and support aimed at special needs caregivers, (although sponsors and DC specialists both underestimated this interest).

- 86% of participants said they are somewhat/very interested in getting help maximizing their benefit dollars across retirement savings, health savings accounts, health care insurance, and voluntary benefits.

Retirement preparedness

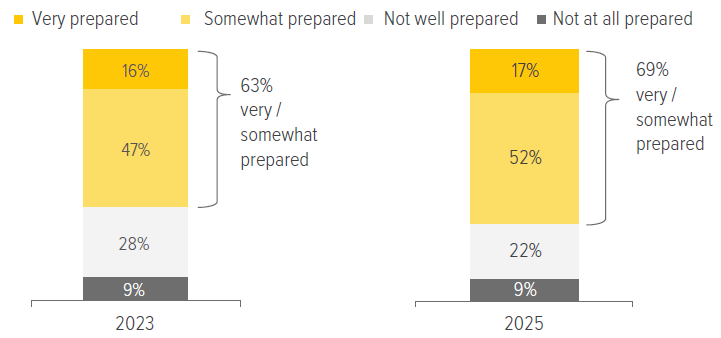

Participant retirement readiness has improved since our last survey. 69% of those surveyed said they feel very or somewhat prepared for retirement—a 6% increase from 2023.

However, participants’ concerns about the impact of inflation and the state of the economy, on their ability to save for retirement also increased this year. 57% reported that these two factors will have a severe/major impact, up from 53% in 2023. Women were significantly more likely than men to believe that the economy will have a severe or major impact on their ability to save for retirement (62% versus 53%, respectively).

For the first time, we asked participants about the impact of market volatility on their ability to save for retirement. 29% said it would have a severe or major impact, and this sentiment was significantly higher among men than women (35% versus 23%).

Once again, there was a meaningful gender gap in feelings of retirement readiness, with women significantly less likely to feel prepared than men (58% versus 79%, respectively).

Working with a financial advisor boosted confidence among participants: Those working with an advisor were 25% more likely to indicate they were very or somewhat prepared for retirement than those who did not have an advisor.