Global Perspectives: Shifting U.S. and International Trends

CIO, Multi-Asset Strategies and Solutions

In 2025, the U.S. economy has shown resilience despite challenges from government policies. While inflation has eased, it remains elevated due to ongoing tariff-related pressures, and the labor market is in a period of low hiring, low firing.

Executive summary

In 2025, the U.S. economy has shown resilience despite challenges from government policies. While inflation has eased, it remains elevated due to ongoing tariff-related pressures, and the labor market is in a period of low hiring, low firing.

While these forces may challenge markets in the near term, strong U.S. earnings growth, durable balance sheets among large cap companies, and stock buyback activity are supporting equities. Looking ahead, we expect innovation, productivity growth, and lower interest rates will reinforce U.S. economic leadership—making large company stocks and high-quality bonds attractive options.

Third quarter 2025 market performance

Markets rallied in 3Q25, primarily fueled by resilient U.S. corporate earnings, growing investor optimism surrounding AI-driven productivity gains, and increasing expectations for monetary easing by the Federal Reserve. Inflation rose slightly over the quarter, largely due to tariff-driven price pressures on goods, which offset easing inflation in the services sector. In response, the Federal Reserve implemented its first interest rate cut in a year and signaled the possibility of further reductions. This policy shift provided a significant boost to equities, especially benefiting small cap stocks, which are typically more sensitive to lower interest rates. Among large cap equities, growth stocks outperformed value stocks, with the technology and communications sectors once again leading market gains.

International developed equities posted modest gains during the quarter, although sentiment remained subdued due to ongoing political uncertainty and lackluster productivity growth. After a particularly strong performance in the first half of the year, European markets lagged, largely attributable to underperformance in Germany and France, where U.S. tariffs negatively impacted exports and reduced output in key manufacturing sectors. Additionally, political instability in the region caused some investors to question Europe’s fiscal flexibility. Japan, on the other hand, delivered strong returns as Prime Minister Shigeru Ishiba resigned, raising expectations for more supportive policies. Inflation moderated and the yen weakened, further supporting Japanese equities.

Emerging markets outperformed, with China standing out as a key driver of growth. In China, targeted government stimulus measures, expansion in AI-driven industries, and robust earnings in the technology sector helped offset deflationary pressures and property market weakness, attracting increased domestic capital.

Fixed income markets generated positive, albeit modest, returns for the quarter that lagged behind those of equities, largely due to persistent inflation and continued policy uncertainty. Both investmentgrade and high-yield credit remained supported by strong fundamentals; however, historically tight spreads limited the potential for further upside. Long-duration bonds benefited from the growing expectations of additional interest rate cuts by the Federal Reserve.

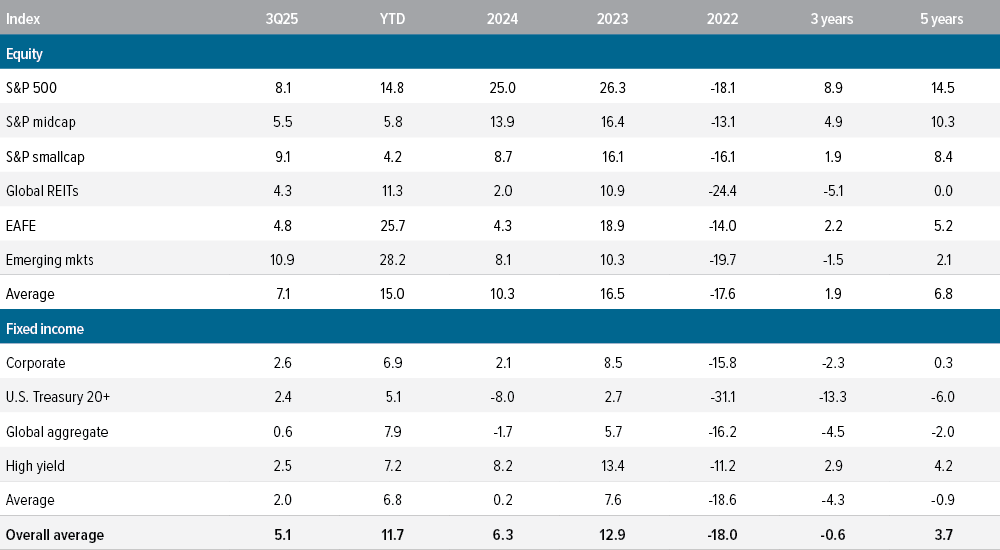

As of 09/30/25. Source: FactSet, FTSE NAREIT, Morningstar, Voya Investment Management. The overall average model allocation includes 10 asset classes, equally weighted: S&P 500, S&P 400 Midcap, S&P 600 Smallcap, MSCI U.S. REIT Index/FTSE EPRA REIT Index, MSCI EAFE Index, MSCI BRIC Index, Bloomberg Barclays U.S. Corporate Bonds, Bloomberg Barclays U.S. Treasury Bonds, Bloomberg Barclays Global Aggregate Bonds, Bloomberg Barclays U.S. High Yield Bonds. Returns are annualized for periods longer than one year. Past performance is no guarantee of future results. An investment cannot be made in an index.

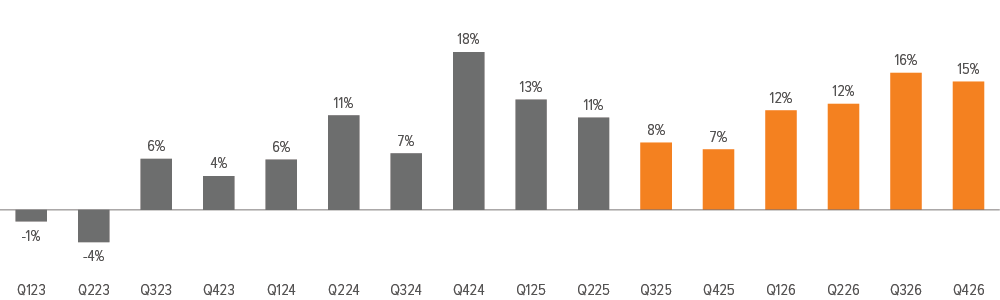

2Q25 YoY S&P 500 corporate earnings stay positive

For the quarter ending June 30, 2025—earnings reports finished in September 2025—the YoY earnings growth for the S&P 500 companies was 13.8%. Eight out of 11 sectors delivered positive growth. Communications, technology, and financials sectors led the way, with earnings each rising by double digits, compared with this time last year. Energy, materials, and utilities sectors’ earnings declined during the period. In aggregate, reported earnings were better than expectations as more than 80% of companies beat.

Market outlook

Inflation has made notable progress over the past few years, with the core personal consumption expenditures (PCE) halving from a cycle high of 5.6% in September 2022 to a 12-month average of 2.8%. Services inflation remains the key driver of overall price pressures. However, recent declines in shelter and transportation services suggest a more constructive trend.

Despite the encouraging developments, the outlook for inflation warrants caution. Tariffs are projected to rise from 12% to 19% by year-end, which may have a more pronounced effect on consumer prices. While goods prices may continue to rise in the near term due to these tariff pressures, we believe the effects will be short-lived. Unlike during the pandemic, consumers today are more price sensitive and possess less discretionary spending power, which is likely to dampen demand and limit the persistence of goods-related inflation.

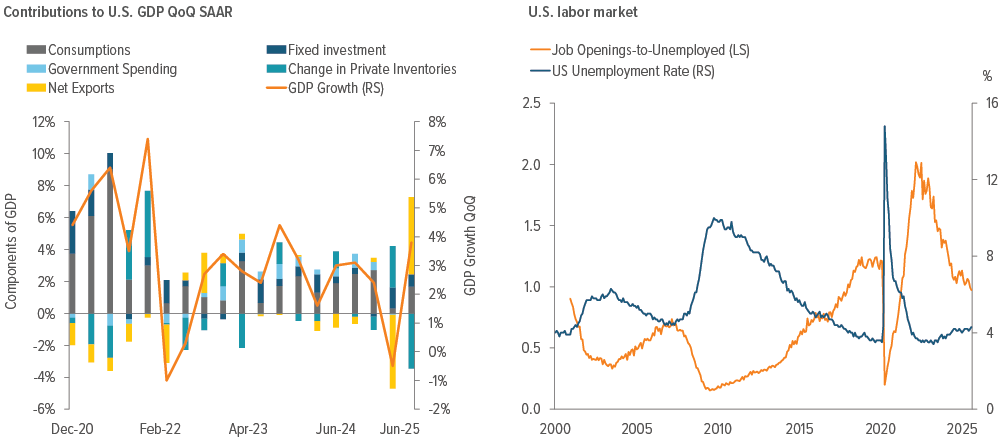

Since economic activity is highly dependent on the consumer, we are watching the labor market closely. The labor market is softening; hiring has slowed and the ratio of job vacancies to unemployed persons continues to decline (Exhibit 3). This reduced labor demand is occurring alongside tighter immigration policies and an aging population, which are constraining labor supply. As a result, the breakeven employment point—which is the number of jobs that must be created to keep the unemployment rate steady—is lower. This period of low hiring, low firing will likely last until there is an economic shock. As the Fed ramps up an interest rate cutting cycle, we expect continued U.S. economic resilience with positive but moderating U.S. GDP growth (Exhibit 4).

As of 09/25/25. Source: Bloomberg, Voya IM.

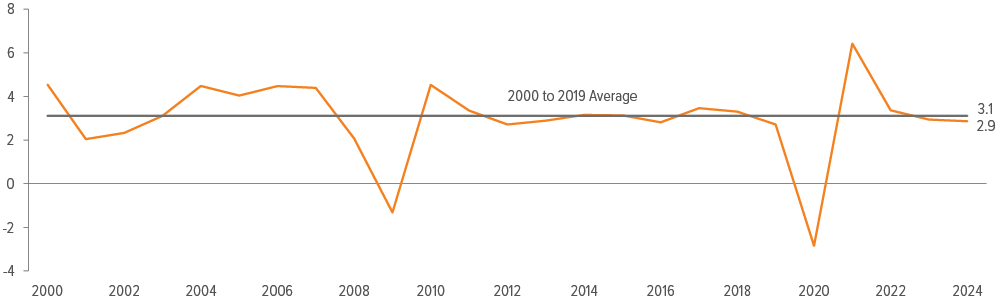

Outside the U.S., momentum is less convincing. Europe has relied on fiscal spending to prop up economic activity, but we don’t think the benefits will last. In addition, multiple countries continue to grapple with political instability, and the region faces intensifying competition from Asia. We see limited catalysts for a sustained acceleration in the region overall. The drags of elevated mortgage costs and higher business taxes are expected to weigh on U.K. consumers and companies for some time. Japan is relatively more attractive, with corporate reforms improving profitability, though political upheaval from Prime Minister Ishiba stepping down and the risk of faster rate hikes may limit upside. China’s recovery, in our view, is a weak link: Property sector stress and wary consumers have muted the impact of policy stimulus, leaving growth below potential and creating a headwind for broader Asia. Trade uncertainty and the country’s regulatory regime also influence investor optimism. At the same time, the offshore China equity market has a different composition than the overall economy and remains heavily overweight technology, a favorable sector in our opinion. Overall, we forecast ~3% global growth this year, which is roughly the average rate since 2000 (Exhibit 5).

As of 12/31/24. Source: Bloomberg, Voya IM.

We believe equities remain more attractive than bonds or cash, led by U.S. large caps, which offer both durable balance sheets and consistent earnings power (Exhibit 6). Within large caps, we maintain a balanced approach. Growth stocks benefit from innovation and AI adoption, while value-oriented companies, particularly financials and industrials, trade at relative discounts and may profit from policy support. The passage of the One Big Beautiful Bill Act (OBBBA) should support U.S. corporate activity by reducing corporate tax liability and potentially boosting investment spending. Small caps, despite a rally this summer, remain more vulnerable to tariffs and financing costs, leading us to favor larger cap companies. Abroad, opportunities are thinner: Europe trades cheaply but lacks earnings momentum; the U.K. faces persistent macro drags; and, while Japanese fundamentals have improved, the rapid rise in inflation and political upheaval warrant caution. We remain neutral on emerging markets. While China equities are at 10-year highs, driven by liquidity and its technology sector, weak economic fundamentals such as soft consumer demand and declining home prices pose risks.

As of 09/10/25. Source: Bloomberg, Voya IM.

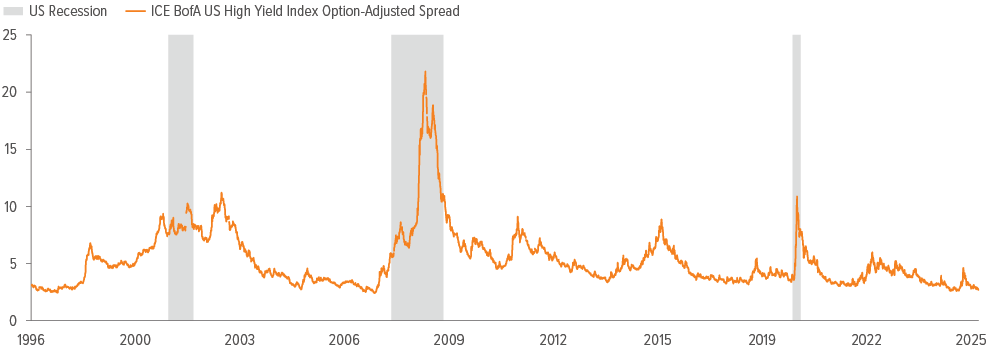

In fixed income, Treasuries remain attractive as a defensive anchor. With real yields currently in the 1.5-2.5% range, investors can access income and diversification opportunities that have been rare over the past decade. Credit spreads are near multi-decade lows (Exhibit 7), leaving carry as the main driver of returns. Given stretched valuations in riskier credit segments, we favor investment grade bonds over high yield. International bonds offer less compelling yields, and emerging market debt is challenged by uneven fundamentals, reinforcing our preference for core U.S. exposure.

As of 09/10/25. Source: Bloomberg, Voya IM.

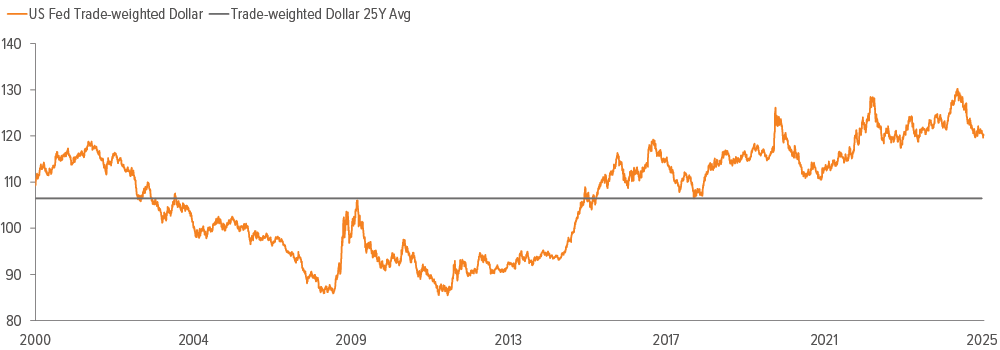

The U.S. dollar has declined by approximately 10% this year against a trade-weighted basket of currencies, yet it remains above its 25-year average (Exhibit 8). Valuation models based on purchasing power parity and real effective exchange rates suggest the dollar remains overvalued. Additionally, slower U.S. growth, expected monetary easing, and persistent trade deficits point to a gradual depreciation. However, the U.S. dollar should retain its safe-haven status during periods of global stress.

Commodities offer a more nuanced story. Oil prices are capped in the mid-$50s to $60s per barrel due to oversupply from OPEC+, U.S., and Latin American producers alongside tepid Chinese demand. In contrast, gold stands out as a hedge and beneficiary of a weaker dollar, while benefiting from central bank demand.

Source: Bloomberg, Voya IM, as of 09/25/25.