Slowing Yet Steady Economic Growth

Barbara Reinhard, CFA

CIO, Multi-Asset Strategies and Solutions

While investors grapple with economic crosscurrents, U.S. corporate earnings remained positive, maintaining our base positioning in our Global Perspectives portfolios.

Executive summary

- The U.S. economy has demonstrated resilience with an average real annual GDP growth of 3.4% since 2021, despite ongoing inflation and significant monetary policy tightening. However, growth is expected to slow for the rest of the year.

- U.S. equities are supported by earnings quality, growth potential and stability amid global economic uncertainties. Meanwhile, high-quality fixed income all-in yields continues to be attractive.

- With U.S. corporate earnings once again positive, Global Perspectives portfolios remain in base positioning

Second quarter 2024 review

U.S. stock and bond markets faced challenges at the beginning of the second quarter, as hot inflation readings dampened expectations for Fed rate cuts. Towards the end of the quarter, however, the outlook improved as favorable May inflation data increased investor confidence in potential Fed rate reductions by September. This, along with continued strength in the labor market and rising earnings optimism, helped broad equity markets post gains for the period. Large cap stocks outperformed small caps, and growth beat value. Within the S&P 500 Index, technology, communication services and utilities sectors led, while materials, industrials and energy lagged.

International stocks also moved higher, with emerging markets (EM) outperforming developed. China and India, the two largest countries within the EM equity index, both performed well. Chinese equities were helped by government support for the real estate sector and improving industrial production, while Indian equities saw strong performance continue after general elections concluded and Prime Minister Modi secured his third term in office. Japanese stocks underperformed in the period primarily due to uncertainty surrounding the Bank of Japan’s monetary policy normalization and the expected appreciation of the yen, which raised concerns about the competitiveness of Japanese exports.

Fixed income markets had mixed performance but declined in aggregate as the U.S. Treasury yield curve rose slightly. High yield bonds performed well due to strong corporate earnings, which pulled spreads tighter. As with international equities, emerging market bonds outperformed developed market issues, as French government bonds dropped on political uncertainty.

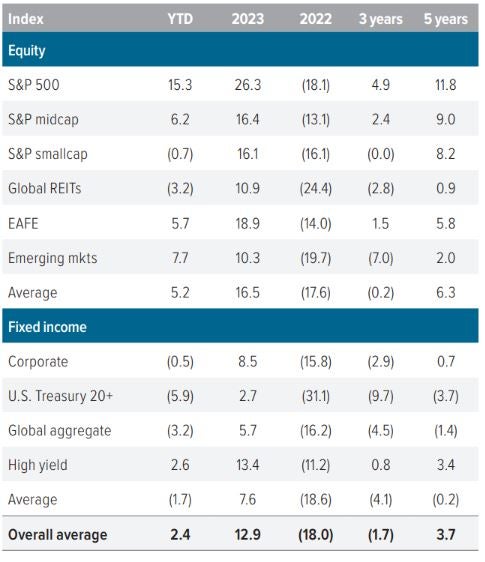

As of 6/30/24. Source: FactSet, FTSE NAREIT, Voya IM. The overall average model allocation includes 10 asset classes, equally weighted: S&P 500, S&P MidCap 400, S&P SmallCap 600, MSCI U.S. REIT Index/FTSE EPRA REIT Index, MSCI EAFE Index, MSCI BRIC Index, Bloomberg Barclays U.S. Corporate Bonds, Bloomberg Barclays U.S. Treasury Bonds, Bloomberg Barclays Global Aggregate Bonds, Bloomberg Barclays U.S. High Yield Bonds. Returns are annualized for periods longer than one year. Past performance is no guarantee of future results. An investment cannot be made in an index.

Macro environment: Slower but steady at the surface

Following persistent inflation and significant monetary tightening, the stamina of the U.S. economy has been remarkable. Since 2021, real annual GDP growth has averaged 3.4%, versus the 2.4% from 2010 to 2019. At the same time, the unemployment rate has averaged 4.3% in the post-pandemic period, versus 6.3% in the post-GFC period.

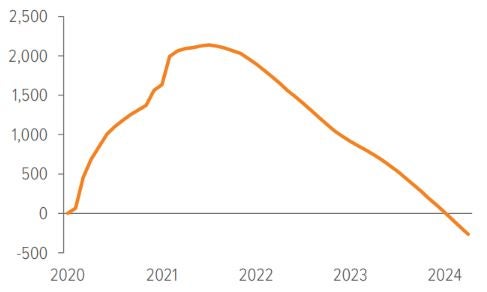

However, the demand-side effect of high interest rates is becoming increasingly apparent as excess savings have been depleted (Exhibit 2) and evidence continues to support our view that growth will be below trend and exert downward pressure on prices.

As of 05/01/24. Source: Federal Reserve Bank of San Francisco, Bloomberg, U.S. Bureau of Labor Statistics, Voya IM.

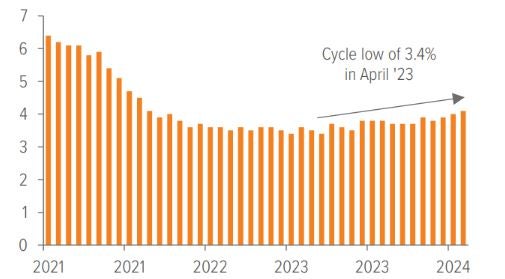

U.S. real GDP growth declined to 1.4% in 1Q24 from 3.4% in the prior quarter, and the unemployment rate rose for the fifth consecutive quarter to 4.1% in June (Exhibit 3).

Contracting employment components in ISM PMIs also indicated employment’s softening trend, but a surprising increase in job openings to 8.1 million in May suggested cooling rather than a fast freeze. Moreover, a weaker labor market’s effect on the consumer could be somewhat offset by the resumption of disinflationary trends, which should support real incomes at a level consistent with 2% inflation.

As of 06/30/24. Source: Bloomberg, Voya IM.

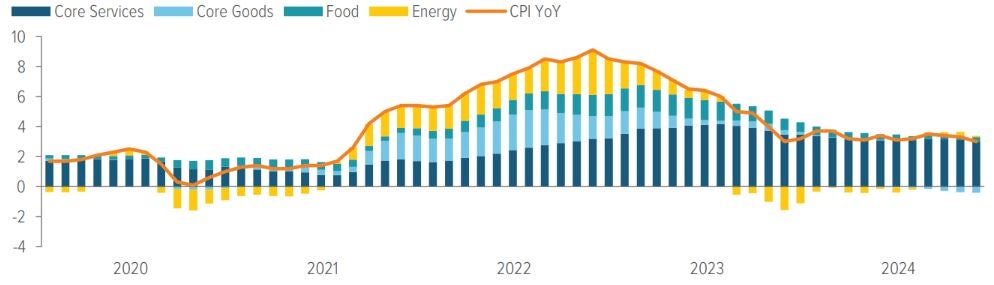

Fortunately, after several hotter-than-expected readings in the first quarter, inflation has resumed its descent; the Consumer Price Index (CPI) fell for the fourth straight month—to 3.0% YoY—in June (Exhibit 4). Core CPI declined to 3.3%, as goods inflation turned negative, but remained above pre-pandemic levels on elevated services prices. Importantly, shelter prices, the biggest driver of services inflation, experienced their smallest monthly increase since August 2021. This welcome news seemed to confirm the efficacy of the Fed’s policy and align with our economic forecasts.

As of 06/30/24. Source: Bloomberg, U.S. Bureau of Labor Statistics, Voya IM.

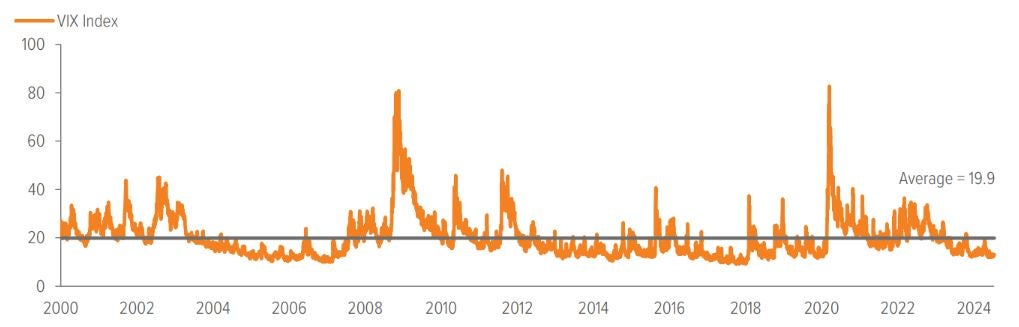

Given the normalization in supply chains and a rebalanced labor market toward pre-pandemic levels, we believe prices will drift lower without unemployment leaping higher. We expect the U.S. to continue to grow and stay out of a recession over the next 12 months. Our belief is that pullbacks will be short-lived and a significant decline in equity markets isn’t likely. However, this view doesn’t suggest that there is significant upside to equities markets in the near term. In fact, the impending U.S. election may cause a pickup in equity volatility from currently low levels (Exhibit 5).

As U.S. investors grapple with potential economic crosscurrents characteristic of a late-cycle environment, we maintain a neutral posture between stocks and bonds that balances their competing inherent risks.

As of 07/16/24. Source: Bloomberg, U.S. Bureau of Labor Statistics, Voya IM.

1Q 2024 YoY S&P 500 corporate earnings stay positive—GP portfolios remain in base allocations

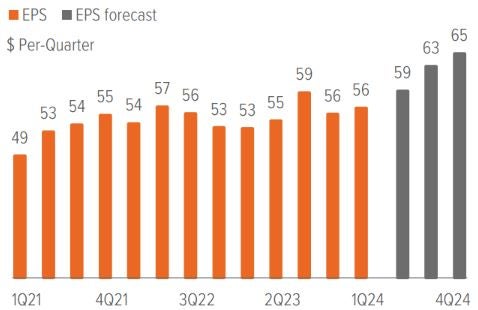

S&P 500 first-quarter earnings grew by 8.2% yearover-year, with 8 of the 11 sectors showing increases from a year before. The communication services, consumer discretionary and technology sectors led the way, with earnings rising by 43%, 28% and 26%, respectively, compared with 1Q last year. Energy, materials and healthcare sectors’ earnings all declined during the period. In aggregate, earnings came in better than expected with 79% of companies beating. With U.S. corporate earnings once again positive, Global Perspectives portfolios remain in base positioning (Exhibit 6).

U.S. equities: Back to the well as winners poised to keep winning

The current global economic landscape and market dynamics suggest strategic positioning that favors U.S. assets—specifically large cap stocks. The U.S., which is in a better economic situation than much of the rest of the world, has become a global destination for investor flows. Given its relatively stable economic conditions, technological innovation and strong financial markets, we have good reason to believe this will continue. As a result, the U.S. is our favored region.

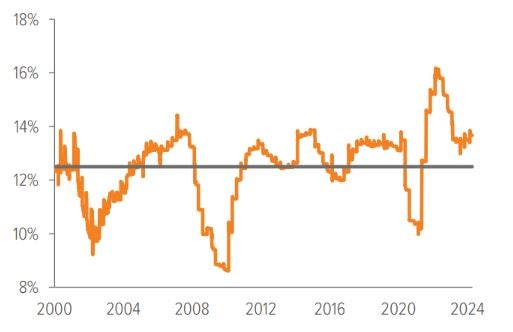

We think large cap stocks are particularly appealing due to their earnings quality, growth potential and momentum. However, we recognize that earnings expectations are somewhat extended (Exhibit 7). With nominal GDP growth falling, meaningful upside to sales growth will be difficult, but solid profit margins (Exhibit 8) and high returns on equity should continue to support valuations.

While pressure to maintain their earnings growth trajectory is high, U.S. technology mega-caps are facing scrutiny on artificial intelligence spend. For example, hyperscalers—including Amazon, Meta, Microsoft and Alphabet—have spent about $360 billion over the past year.1 Eventually, these firms will need to prove their investments will generate revenues and earnings, but companies need time to move from training models to production before accurate assessments can be made, and results aren’t required yet. Meanwhile, AI infrastructure providers—such as those supplying chips, memory and servers—are producing massive cash flows. We also like the overall stability of large companies as a buffer against global economic and geopolitical uncertainties, and we believe they continue to offer a compelling risk/reward opportunity

As of 07/16/24. Source: FactSet, Bloomberg, U.S. Bureau of Labor Statistics, Voya IM.

International equities: Challenges offset optimism and hope

International stocks present mixed prospects.

Japan is struggling with a weak currency and challenges in normalizing monetary policy, despite potential rate hikes influenced by easing U.S. inflation and European Central Bank cuts.

Europe faces sluggish growth due to high labor costs, persistent core inflation and geopolitical tensions, exacerbated by domestic political instability (particularly in France).

In contrast, the U.K. appears more stable and attractive to investors, buoyed by political shifts (victory for the Labour Party under Sir Keir Starmer), anticipated Bank of England rate cuts, and favorable macroeconomic data.

Meanwhile, China’s stock market has rallied, driven by strong GDP growth and healthy manufacturing sectors (e.g., electric vehicles and industrial robotics). However, significant risks linger due to its ongoing property crisis and sensitive international relations, especially with the U.S.

Fixed income: Comfort in quality

We maintain our preference for higher quality within fixed income. Despite limited upside potential due to already tight spreads, the supportive macroeconomic environment underpins solid corporate fundamentals, making the additional yield from investment grade bonds a worthwhile risk. Securitized credit products, particularly consumer-oriented asset-backed securities and residential mortgage-backed securities, appear attractive. Additionally, a beaten-down CMBS sector appears to offer value opportunities for savvy security selectors. Despite higher interest costs beginning to weigh on credit quality in the high yield space, defaults and credit stress remain limited. However, increasing tail risks keep us neutral.

We don’t have strong conviction on the near-term direction of rates but do hold a modest long duration posture in more aggressive, equity-heavy portfolios to provide added ballast to higher beta. We prefer nominal bonds over real bonds to hedge against the downside in equity returns. With some foreign central bank rate cutting cycles already underway, certain countries’ bond markets look interesting, however, when considering the support for a strong U.S. dollar and the potential negative currency impacts, we remain underweight non-U.S. bonds.

A note about risk

Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. All investments are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.