Securitized credit isn’t complicated. It’s an investment involving predictable consumer behaviors that have fueled economic growth for generations.

Consumers are the engine of the U.S. economy

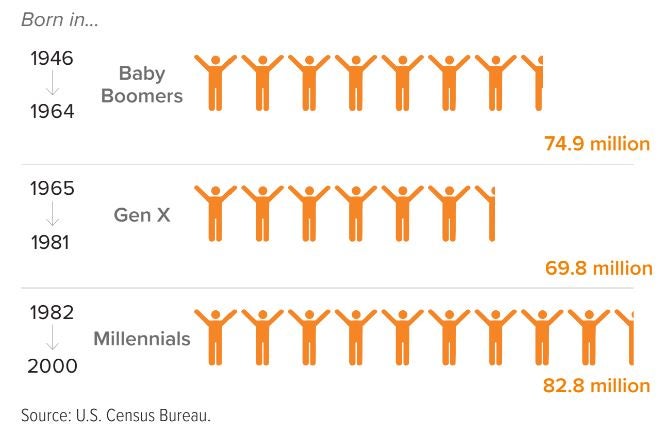

Right now, nearly 83 million Millennials (ages 20– 40) in the U.S. are transitioning to the next phase of their lives. Meanwhile, 75 million Baby Boomers (ages 56–75) are entering their golden years of retirement. People in each demographic will have to live somewhere, do things and buy goods and services.

Over time, U.S. consumers have been very predictable. Personal consumption makes up about two-thirds of U.S. gross domestic product, or $18.6 trillion.1 That’s larger than the total GDP of China or the combined GDP of Japan, Germany, the United Kingdom and India.

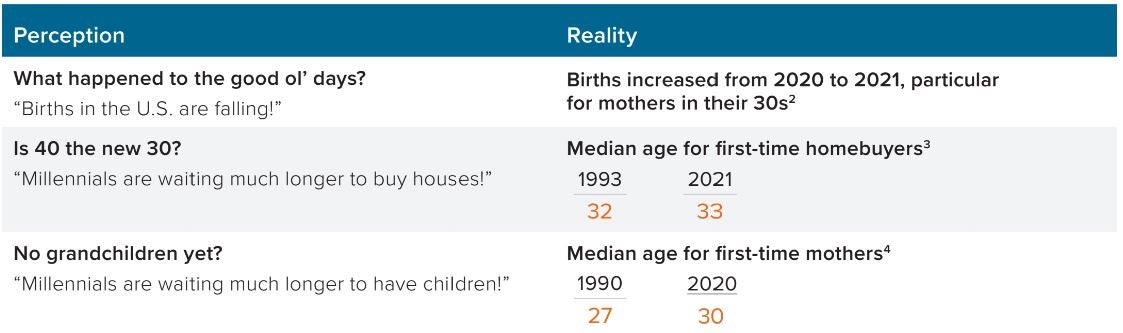

The U.S. consumer is an economic force. Yet we often see a negative picture painted that cites longer-term declines in household formation and shorter-term challenges like inflation. But there’s perception, and then there’s the reality of cold hard facts…

Through generations, U.S. consumer behavior has proven to be not only predictable, but a key catalyst for ongoing economic expansion. Despite wars, periods of stagflation, geopolitical turmoil and recessions, demographic trends have held steady over time. For example, 4 out of 5 Americans have children in their lifetimes.5 This predictable action forces behavior that drives economic activity. Once a child is born, we don’t really have a choice—we have to spend money, because kids need things. As of 2023, it cost the median household in America $374,634 to raise a child from birth to age 17 (and that doesn’t include college).6

What does this have to do with securitized credit?

Securitized credit is an investment in everyday life.

Securities backed by loans, mortgages and other assets aren’t complicated. They revolve around basic activities that move the economy forward. One party enters into a credit contract with another party, agreeing to specified repayment terms. That contract is pooled with similar contracts to serve as collateral and generate cashflow for different types of securities. Although the specific type of collateral is different across each flavor of securitized credit, the strength (or lack thereof) of the U.S. consumer is the overarching driver of risk and reward potential in the space.

| Where you LIVE | What you DO | What you BUY | |

|---|---|---|---|

|  |  | |

| Activity | Buy a home | Work at an office or start a new business | Buy goods on a credit card or lease a car |

| Contract | Pay a mortgage | Pay a mortgage or bank loan | Make a credit card or lease payment |

| Collateral | Cashflow from a group of residential mortgages | Cashflow from a group of commercial mortgages or bank loans | Cashflow from a group of loans |

| Issued as... | Residential mortgage-backed securities (RMBS) | Commercial mortgage-backed securities (CMBS) or collateralized loan obligations (CLOs) | Asset-backed securities (ABS) |

Remember, securitized credit investments are an output of where you live, what you do and what you buy. As people live life within these three buckets, there tends to be more issuance of securitized credit. And, as a crucial corollary, if consumers are judged to have the capacity and willingness to repay, they are likely to meet their contractual agreements and maintain cash flows in the collateral pools of securitized credit.

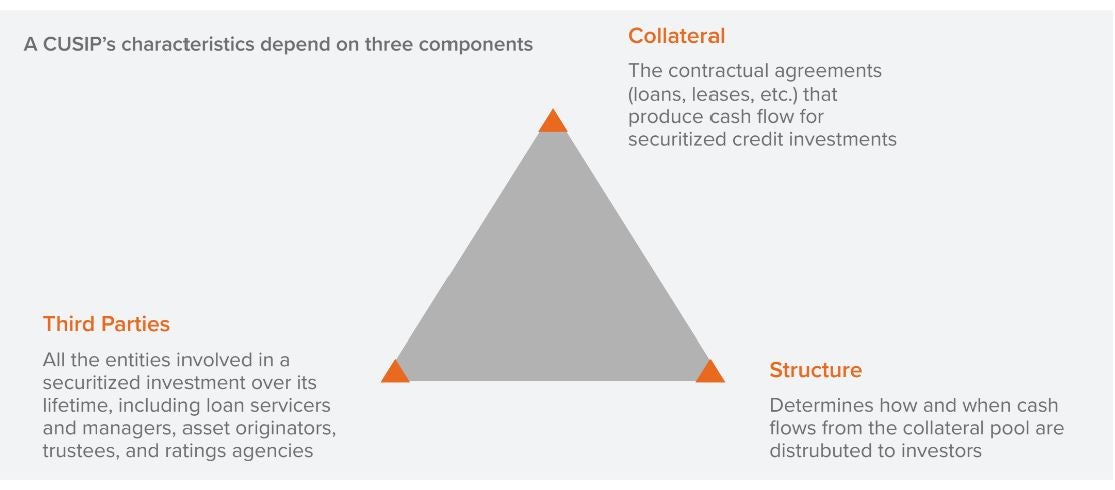

A story behind every CUSIP

Where things get tricky with securitized credit is that two investments in the same subsector (say, CMBS) can produce dramatically different returns. Why? Each security, identified by a unique CUSIP, is defined by three key components: the collateral, the security structure and third-party relationships (see below). These three factors determine important things like what happens if borrowers in the collateral pool pay off early, or what happens if the underlying assets experience a decline in value.

The research necessary to understand and monitor changes in these components requires experience and resources. Active managers such as Voya may deploy extensive fundamental research capabilities to identify investments that offer attractive potential across the securitized market, including ABS, RMBS, CMBS and CLOs.

Securitized credit is a “through-the-cycle” allocation

Regardless of the state of the economy, people will get married, have children and buy homes. This household formation drives financing needs and is a powerful driver of investment opportunity. With its underlying collateral closely connected to predictable U.S. consumer activity, securitized credit offers a vital source of potential income, returns and diversification within a broader fixed income portfolio.

To learn how securitized credit can enhance your existing portfolio, contact your Voya IM representative or read more at voyainvestments.com.