Ethereum: Building the Backbone of Digital Finance

Senior Portfolio Manager and Equity Analyst

Head of Global Technology

Portfolio Manager and Equity Analyst

Senior Client Portfolio Manager, Thematic Equities

Key Takeaways

Ethereum’s trajectory—from smart contract pioneer to global settlement and tokenization platform—suggests a durable role at the center of digital markets.

As individuals, corporations, asset managers, and public institutions adopt on-chain workflows and tokenized assets, Ethereum’s network effects deepen, creating a reinforcing cycle of liquidity, utility, and innovation.

In our view, Ethereum is not merely an asset to allocate to—it is core infrastructure for a programmable financial future.

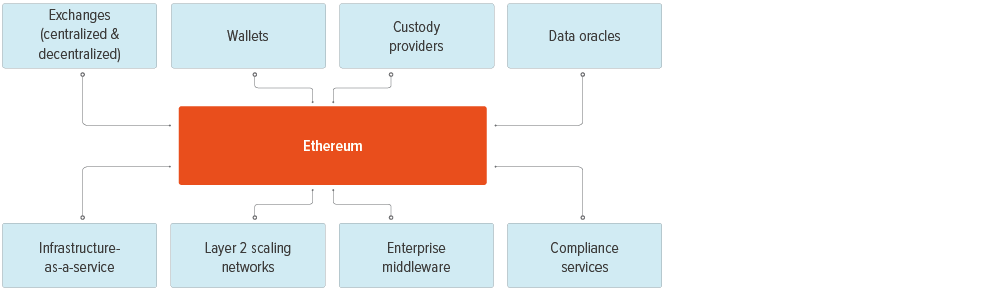

Ethereum’s evolution from an idea to a powerful and versatile platform is reshaping how financial services are built, delivered, and owned. Behind it is a whole value chain for investors to consider.

Since its launch in 2015, Ethereum has evolved far beyond a simple blockchain. What started as an experiment in programmable money is now a foundation for smart contracts, decentralized finance (DeFi), tokenized assets, and thousands of on‑chain applications. Over time, Ethereum has shifted from being a “crypto project” to something more like financial and computing infrastructure that institutions, developers, and even governments are beginning to rely on.

In looking at Ethereum’s long‑term potential, three themes stand out:

1. A programmable platform with a strong community

Ethereum’s design makes it relatively straightforward for developers to build automated programs, or “smart contracts,” that run independently once deployed.

What makes Ethereum unusual is the size and energy of its developer base—the largest in the crypto ecosystem.1 This matters because applications are more useful when they can interconnect: Lending protocols plug into exchanges. Payment platforms tie into wallets. And stablecoins move seamlessly between them. Ethereum benefits from these network effects and is increasingly serving as the base settlement layer for digital assets, payments, and even digital identity.

2. Scaling for real-world use

One criticism of Ethereum has always been that it doesn’t scale well. Fees can spike during busy periods, making regular transactions costly. The roadmap addresses this with so‑called “Layer 2” networks. These are essentially parallel highways that let traffic move faster and cheaper while still anchoring back to Ethereum’s core security. Optimistic and Zero‑Knowledge (ZK) rollups, for example, batch thousands of transactions and settle them back to the main chain.

Combined with upgrades that reduce data posting costs, this scaling approach is starting to make Ethereum viable for everything from institutional finance to microtransactions in games or web apps.

3. Integration and disruption of traditional finance

Perhaps the most striking development over the last few years has been the move from early-stage pilots to actual deployment by large financial institutions.

Treasury bills, money‑market funds, and even private assets are being tokenized and settled on Ethereum or its scaling networks. At the same time, regulators have given more clarity on custody, tokenization, and compliance requirements, which makes it easier for banks and asset managers to get involved.

But beneath the surface, Ethereum does more than just “integrate” with existing finance—it alters its fundamental economics:

- Settlement that traditionally takes days can happen in minutes.

- Middlemen that extract fees for clearing, custody, or reconciliation can be automated away by smart contracts.

- Tokenized assets can be traded peer-to-peer, 24/7, without the need for exchanges to maintain exclusive control over order flow.

- For lenders and borrowers, DeFi protocols provide direct access to liquidity that competes with banks.

In other words, Ethereum threatens to shift value away from legacy intermediaries and toward open, programmable networks—making finance more competitive, transparent, and borderless.

Ethereum’s broader role

The story of Ethereum isn’t only about technology—it’s about the ecosystem that grew around it. Developers contribute open‑source tools and keep applications interoperable with standardized token formats, such as Ethereum Request for Comments (ERC), which are community-written technical standards that define how things should work. And liquidity flows through a shared set of rails that support stablecoins, ETH, and tokenized assets alike.

Around that core, an entire commercial stack has emerged:

For investors and builders, this means exposure to Ethereum’s growth doesn’t have to mean owning ETH directly—there’s a whole value chain to consider.

Looking ahead

Ethereum is still adapting. Its architecture increasingly separates roles: security and final settlement at the base layer, while most execution happens across faster rollups and side networks. This layered model balances decentralization with usability. Institutional adoption is growing as tokenized assets, compliant trading platforms, and regulated investment vehicles come online.

But the deeper shift may be structural disruption. As capital markets and payments move on‑chain, traditional financial institutions risk being disintermediated. Clearing houses, brokers, and even banks could find their roles diminished if investors and consumers embrace direct, programmable access to assets and liquidity. Regulators, too, will need to adjust oversight for a world where critical pieces of finance no longer run through centralized entities, but rather global open‑source infrastructure.

Taken together, these developments suggest Ethereum will continue to play a central role in programmable finance. Rather than being just another token to invest in, Ethereum is steadily becoming digital infrastructure that both partners with and challenges traditional finance—building the rails for payments, asset settlement, and on‑chain applications that operate around the clock and across borders.

A note about risk: Investing in cryptocurrencies and cryptocurrency-related companies involves risks which include, but are not limited to: Market volatility: Cryptocurrencies are known for their extreme price volatility. The value of cryptocurrencies can fluctuate widely within a short period, leading to potential significant losses for investors. Regulatory uncertainty: The regulatory environment for cryptocurrencies is rapidly evolving. Changes in laws and regulations can impact the legality, use, and value of cryptocurrencies. Investors should be aware of the legal status of cryptocurrencies in their jurisdiction and any potential regulatory changes that could affect their investments. Liquidity risks: The liquidity of cryptocurrencies can vary significantly. Some investments may have low trading volumes, making it difficult to buy or sell large amounts without affecting the market price. This can result in unfavorable trading conditions and potential losses. Operational risks: Cryptocurrency exchanges and platforms may experience technical issues, outages, or security breaches. These operational risks can disrupt trading activities and lead to financial losses for investors. Legal and compliance risks: Cryptocurrency-related companies may face legal and compliance challenges, including regulatory investigations, enforcement actions, and litigation. These risks can impact the company’s operations, reputation, and financial stability.

Investors should carefully consider these risks and seek professional advice before investing in cryptocurrencies or cryptocurrency-related companies. It is important to stay informed about the latest developments in the cryptocurrency market and regulatory landscape.