Fixed Income Perspectives: Rate Cut Doesn’t Change Much

Head of Multi-Sector Fixed Income

While the Fed’s recent rate cut is grabbing headlines, the relative value landscape hasn’t changed, and we continue to favor securitized over corporate credit.

Rate cut comes in as expected

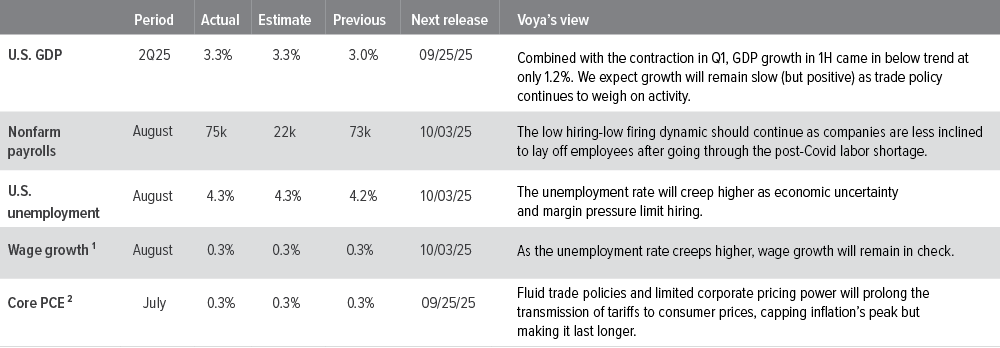

In a move that was largely expected by the market, the Federal Reserve lowered the federal funds rate by a quarter percentage point to 4% from 4.25%. In his press conference, Fed Chair Jerome Powell said, “The labor market is really cooling off,” which aligns with the “low hiring, low firing” view of employment we discussed in detail last month. Like the Fed, we do not see signs that we’re headed toward a masslayoffs phase of a labor market breakdown, but underlying tremors are becoming more evident, particularly at the margins.

Assessing relative value

The Fed’s comments and rate cut announcement do not change our view of relative value in fixed income. Corporate credit spreads remain near multi-decade tights and with spreads failing to fully compensate for taking risk, we prefer to stay up the quality spectrum with a bias toward shorter-dated corporate bonds. In addition, we remain cautious toward lower-quality corporate issuers, where signs of strain are starting to emerge.

From a relative value perspective, as we explored in our recent market update, the securitized markets appear to be well positioned to benefit from the lower rate environment. Agency RMBS markets received a proactive bump in August as markets anticipated the Fed’s recent cut, resulting in a recent move to an underweight stance across portfolios.

The potential benefits of lower rates also extend to non-agency mortgage sectors, both residential and commercial. In each sub-sector, the prospect of lower policy rates translating into lower rate volatility and easier financial conditions has positive implications for prepayments and structural de-leveraging in these important sectors for securitized credit allocations.

Securitized credit outlook 2H25: Keep calm and carry on

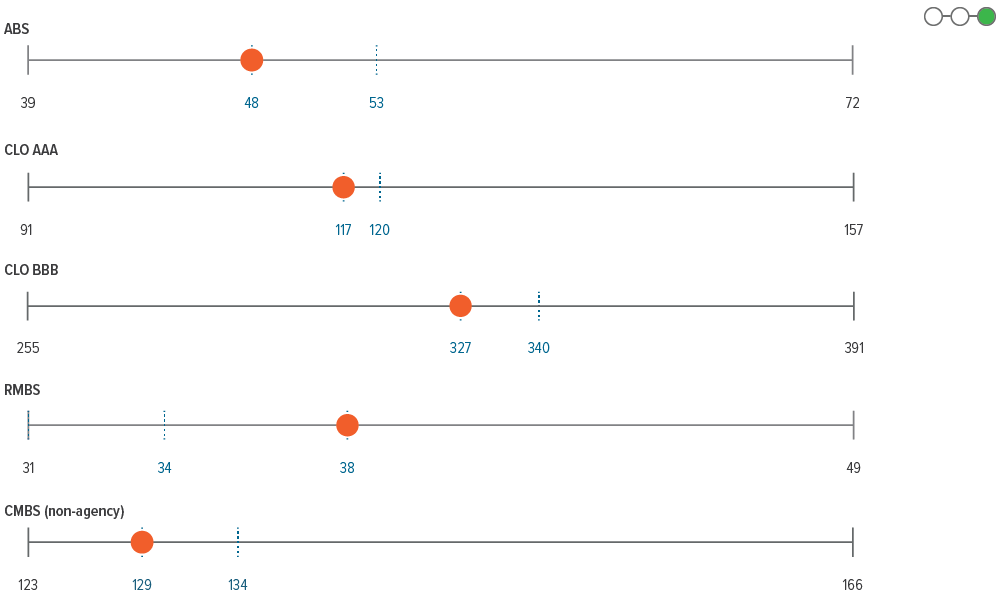

More broadly, securitized credit remains relatively unaffected by the macroeconomic factors like tariffs, the budget deficit, and geopolitics—especially in relation to other corners of the fixed income universe. Our 2H25 securitized market outlook explains why we generally favor the middle of the securitized credit capital stack, BBB+ to A, navigating between safer but duration-heavy AAAs and the riskier cash flows at the low end of the market.

At the sector level, we’re most bullish on commercial mortgage-backed securities in the second half of 2025, as the sector is early in its credit cycle, new issuance is hot, and spreads still have room to tighten.

As of 08/31/25. Source: Bloomberg, FactSet, Voya IM.

* Note: In September, the Fed lowered its target range to 4.00% – 4.25%. As of 08/31/25. Sources: Bloomberg, JP Morgan, Voya IM. See disclosures for more information about indices. Past performance is no guarantee of future results.

Sector outlooks

- 2Q25 corporate earnings are solid so far, with tariffs having the most notable impact in consumer discretionary, where companies missed expectations and guided down more than in other sectors.

- August supply of $100bn was 8% higher than average but in line with expectations.

- We continue to keep IG risk low as spread have moved back to the low end of their historical range given continued solid fundamentals and light supply. From a sector perspective, we prefer financials and utilities over underweight industrials, where we are leaning away from sectors with exposure to M&A risk, trade policy uncertainty.

- On the back of strong earnings and a favorable technical backdrop, high yield is positioned to continue to trade sideways in the near term.

- From a fundamental perspective, the backdrop is moderating due to policy uncertainty, and the risk of policy error-driven weakness raises the risk for cyclicals.

- The magnitude of uncertainty in the market backdrop favors defensive business models and balance sheets, particularly at compressed spread levels.

- The overall carry should continue to boost performance on both a total return and excess return basis, and we are continuing to pay close attention to the evolving developments on the policy and macro front.

- While primary market activity was notably lower compared to July’s record pace, it was still relatively active when looking at historical norms, as August is typically a very quiet month.

- Loan borrowers, especially lower rated and highly leveraged issuers that have faced the immediate transmission of higher rates should experience some reprieve as rates decline.

- Despite the potential for more market volatility on the horizon and technical moves in the mortgage space, we believe carry remains attractive.

- Overall, fundamentals and a favorable technical backdrop are expected to bolster agency mortgage returns going forward, and the Fed rate cut provides a strong technical tailwind for levered players in the space.

- However, near term performance can easily be swayed by large one-off trades from fast money and/or international investors.

- Elevated real yields and softer domestic conditions suggest many EM central banks have room to continue cutting rates, but external factors may limit their flexibility.

- Corporate fundamentals remain resilient, and financial policy remains prudent.

- EM corporates are expected to be indirectly impacted by tariffs through global growth, inflation, and commodity prices. We expect direct impacts to be limited.

- At a time when corporate credit spreads are tighter than ever, securitized markets offer attractive relative value.

- Following recent underperformance, the solid fundamentals in ABS leave the space less prone to drawdowns, giving the sub-sector an avenue to outperform in the near term.

- Broadly speaking, the lower rate environment should support CMBS and RMBS.

- Looking at each space, we are bullish on CMBS as the sector is early in its credit cycle, new issuance is hot, and spreads still have room to tighten. Meanwhile, strong mortgage credit fundamentals and improved valuations should enable RMBS to overcome pockets of weakness emerging in the housing market.

- Weakening technicals and fundamentals make the CLO space susceptible to underperformance. We maintain a heavy bias toward high-quality managers and strong underlying collateral pools.

Glossary of terms OAS: option-adjusted spreads ABS: asset-backed securities CMBS: commercial mortgage-backed securities RMBS: residential mortgage-backed securities CLO: collateralized-loan obligations PCE: personal consumption expenditure YTM: yield to maturity |