Strong relationships with fund sponsors (GPs) can open doors to attractive opportunities and positively influence investment outcomes for secondaries investors. Here’s how.

Strategic relationships can drive strong returns

In secondary private equity, investors don’t just buy into portfolios—they buy into the discipline and decision-making of the managers (GPs)1 behind them. Gaining access to top-quartile funds often depends on knowing the GPs who sponsor them. Building long-term relationships with the top GPs can take years, but it can meaningfully influence long-term results.

Private equity (PE) fund managers add value by improving the performance of companies in their portfolios—at least, that’s the idea. In truth, the skill they bring to drive performance varies widely across managers. Historically, the gap between top- and bottom-quartile PE managers has been wide—ranging from -10% to +46% (Exhibit 1). Compare that with global stock managers, where the range has been much narrower, from 4% to 15%.3

Exhibit 1: In private equity, top managers have historically outperformed by significant margins

Performance differential for the manager universe managers

Global stocks source: Morningstar U.S. Global Large Stock Blend OE Funds for 10 years ending 09/30/25. The large-stock blend universe includes 240 funds, which are ranked based on their annualized returns at the maximum, 75th percentile, 50th percentile, 25th percentile, and minimum levels. Primary buyouts source: Preqin. Data represents all private equity buyout funds in Preqin database as of 11/6/2025 with listed vintages between 2010 and 2019 (post-2019 vintages omitted due to immaturity) and reported performance as of 12/31/24 or later. Funds are ranked based on their net internal rate of return at the maximum, 75th percentile, 50th percentile, 25th percentile, and minimum levels. Past performance is no guarantee of future results, and the possibility of loss does exist. Investments in less liquid private market strategies are by nature risky and typically involve a high degree of leverage. The returns indicated above are long-term and represent well-known asset class indexes and are not meant to be predictive of the performance of any particular fund, nor are they meant to suggest that all private funds result in positive returns or would avoid loss of principal.

The power of partnership: A two-way street

Beyond potential access to top-tier managers, strong relationships between GPs and secondaries fund managers can yield an edge, with value from these relationships flowing both ways.

The above is being provided for illustrative purposes only and represents a sample of potential ways in which primary and secondary managers may work together. Source: Pomona Capital.

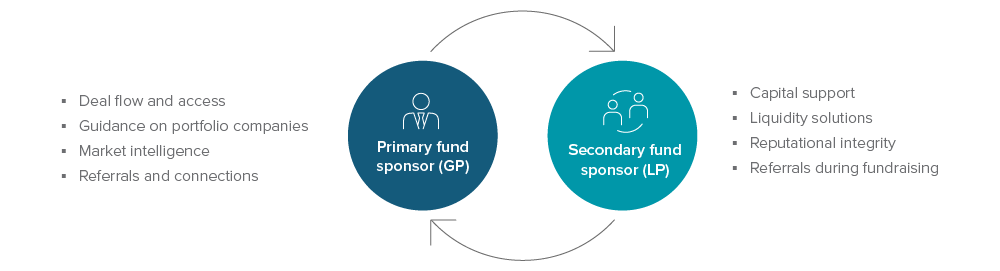

What GPs bring to the table

1. Deal flow and access: GPs connect investors with existing LPs seeking liquidity and may invite trusted investors to participate in preferred opportunities or continuation vehicles. Any transfer of interest to a secondary investor must be approved by the GP, so being a reputable, well-known limited partner can be an advantage.

2. Guidance on portfolio companies: GPs—general partners—often have deep, firsthand knowledge of their underlying portfolio companies, which can yield valuable insights for prospective secondaries buyers. GPs may give early visibility into expected markups before full fund financials are released, how companies are tracking their budgets, or what kind of returns and exit timing might be expected.

3. Market intelligence: Beyond company-level updates, trusted GPs often share their views on the competitive landscape and valuations, offering a broader read on market trends. These insights can be especially useful when navigating uncertain environments or identifying new opportunities.

4. Referrals and connections: Strong relationships can open doors to top-tier GPs and assets in the market.

What LPs give back

1. Capital support: Secondaries investors may also invest as primary limited partners, providing capital throughout a fund’s lifecycle. Their participation is especially important for continuation vehicles, helping drive exits and extend holding periods for prized assets. Secondaries investors that also invest as a primary investor, such as Pomona, can further grow their GP relationships early in a fund’s lifecycle.

2. Liquidity solutions: When LPs desire liquidity, it makes sense that GPs would prefer reputable, known secondaries investors who demand less of their time in facilitating smooth, efficient transfers. Experienced investors expedite the process—they are already familiar with underlying assets so they require less research time. The familiarity of Pomona allows GPs to generate liquidity for LPs who may want to invest in a GP’s latest fund but can’t because their capital is tied up in an earlier fund. Additionally, strong secondaries relationships can help GPs raise continuation vehicles for select assets.

3. Reputational integrity: GPs want their LPs treated fairly and with discretion. Trusted investors help maintain the integrity of portfolio data and foster long-term relationships.

4. References during fundraising: GPs rely on trusted, long-standing relationships to act as references when raising new funds and attracting new investors.

Pomona’s playbook: Diligence meets trust

At Pomona, building relationships involves rigorous diligence of fund sponsors and trust earned through years of experience. The firm sources high-quality GPs through various methods:

- Reviewing a GP’s track record

- Building on prior relationships

- Insights from LPs and placement agents about top-performing GPs

- Gaining conviction by underwriting secondary investments in a GP’s funds

- Conducting research on contacts made through Pomona’s primary program

But it’s not about checking boxes—it’s about knowing the strategy, the team, and what makes each opportunity actionable. Rather than relying on published rankings or one-size-fits-all criteria, Pomona takes a case-by-case approach.

Some GPs are hands-on operators, while others prefer to back well-run businesses and stay out of the way. Pomona works with both. Some GPs are conservative in how they value companies; others are more aggressive. What matters is understanding how each GP works and finding ways to generate strong returns within that framework.

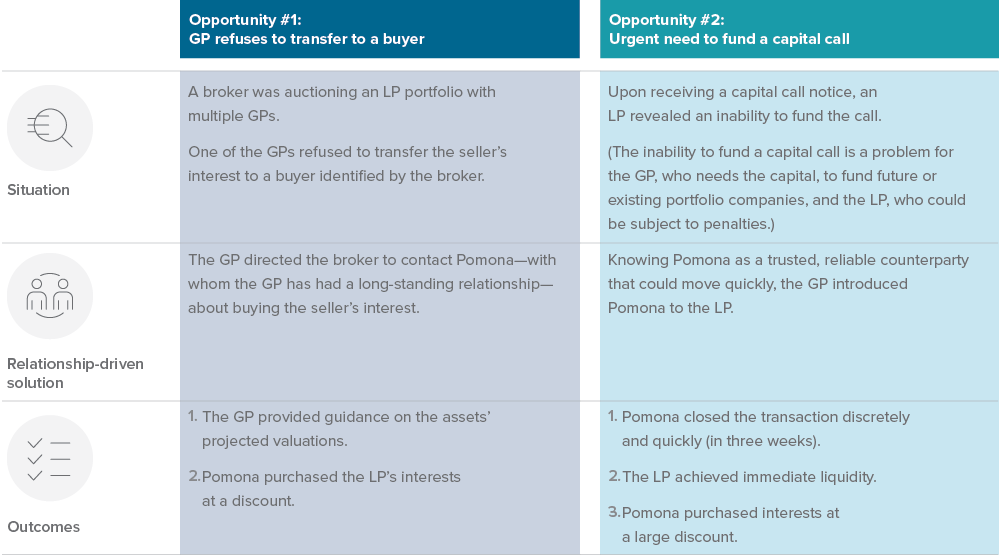

Here are two opportunities that arose due to Pomona’s relationships with GPs:

The above examples are being provided for illustrative purposes only and not all deals in a Pomona-sponsored fund will have the above characteristics.

In private equity secondaries, relationships are more than a competitive edge—they are the foundation of enduring success. The strength of a firm’s connections and the trust it cultivates with GPs and LPs alike determine not only access to opportunities but also investment results. Reputation, built over years of reliable partnership, becomes its own form of capital—one that compounds over time and continues to open doors long after a single transaction closes.

A note on risk:

Secondary investments: The ability of the manager to select and manage successful investment opportunities, underlying fund risks; these are non-controlling investments, no established market for secondaries, identify sufficient investment opportunities, and general economic conditions.

Primary investment: Identify sufficient investment opportunities, blind pool, the manager’s ability to select and manage successful investment opportunities, the ability of a private equity fund to liquidate its investments, diversification, and general economic conditions.

General private equity risks

Investing in private equity is a risk and there is no guarantee that an investment in private equity or in a Pomona sponsored fund will be profitable. The above scenarios are for illustrative purposes only and are theoretical; there is no guarantee an investment in a Pomona-sponsored fund will exhibit any of the above characteristics or return profile. The value of the Fund’s total net assets is expected to fluctuate in response to fluctuations in the value of the Investment Funds, direct investments and other assets in which the Fund invests. An investment in the Fund involves a high degree of risk, including the risk that the Shareholder’s entire investment may be lost.

The Fund’s performance depends upon the Adviser’s selection of Investment Funds and direct investments in operating companies, the allocation of offering proceeds thereto, and the performance of the Investment Funds, direct investments, and other assets. The Investment Funds’ investment activities and investments in operating companies involve the risks associated with private equity investments generally. Risks include adverse changes in national or international economic conditions, adverse local market conditions, the financial conditions of portfolio companies, changes in the availability or terms of financing, changes in interest rates, exchange rates, corporate tax rates and other operating expenses, environmental laws and regulations, and other governmental rules and fiscal policies, energy prices, changes in the relative popularity of certain industries or the availability of purchasers to acquire companies, and dependence on cash flow, as well as acts of God, uninsurable losses, war, terrorism, earthquakes, hurricanes or floods and other factors which are beyond the control of the Fund or the Investment Funds. Unexpected volatility or lack of liquidity, such as the general market conditions that prevailed in 2008, could impair the Fund’s performance and result in its suffering losses. The value of the Fund’s total net assets is expected to fluctuate.

To the extent that the Fund’s portfolio is concentrated in securities of a single issuer or issuers in a single sector, the investment risk may be increased. The Fund’s or an Investment Fund’s use of leverage is likely to cause the Fund’s average net assets to appreciate or depreciate at a greater rate than if leverage were not used. The Fund is a non-diversified, closed-end management investment company with limited performance history that a Shareholder can use to evaluate the Fund’s investment performance. The Fund may be unable to raise substantial capital, which could result in the Fund being unable to structure its investment portfolio as anticipated, and the returns achieved on these investments may be reduced as a result of allocating all of the Fund’s expenses over a smaller asset base.

The initial operating expenses for a new fund, including start-up costs, which may be significant, may be higher than the expenses of an established fund. The Investment Funds may, in some cases, be newly organized with limited operating histories upon which to evaluate their performance. As such, the ability of the Adviser to evaluate past performance or to validate the investment strategies of such Investment Funds will be limited. In addition, the Adviser has not previously managed the assets of a closed-end registered investment company.

Closed-End Fund; Liquidity Risks: The Fund is a non-diversified closed-end management investment company designed principally for long-term investors and is not intended to be a trading vehicle. An investor should not invest in the Fund if the investor needs a liquid investment. Closed-end funds differ from open-end management investment companies (commonly known as mutual funds) in that investors in a closed-end fund do not have the right to redeem their shares on a daily basis at a price based on net asset value.