Mohamed Basma, CFA

Managing Director, Head of Leveraged Credit

Weekly Notables

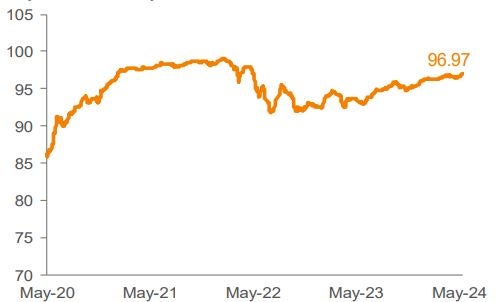

The overall tone was constructive across risk assets this week following the release of the highly anticipated CPI print, which showed inflation easing in April. This had a positive impact on the loan market’s performance, as the Morningstar® LSTA ® US Leveraged Loan Index (Index) returned 0.22% for the seven-day period ended May 16. The average Index bid price continued to move higher, closing out the week at 96.97.

In the primary market, opportunistic transactions continued at a healthy clip given the strong technical backdrop, while a few M&A-related deals were launched as well. MTD volume is already tracking nearly $30 billion halfway through the month. Net of approximately $15 billion of anticipated repayments that aren’t associated with the forward calendar, the amount of net new supply expected to enter the market now totals about $2.1 billion, versus net new supply of $8.1 billion last week.

While trading levels remained firm across all cohorts, performance was led by riskier credits, as BBs, Bs, and CCCs returned 0.22%, 0.20%, and 0.37%, respectively.

Demand for loans was strong across the measurable investor segments. CLO managers issued nine new deals, bringing the YTD tally to $74.2 billion. Retail loan funds experienced $481 million of inflows (Morningstar Direct), extending the streak of positive flows to four weeks and pushing the YTD figure to $5.6 billion (weekly reporting funds).

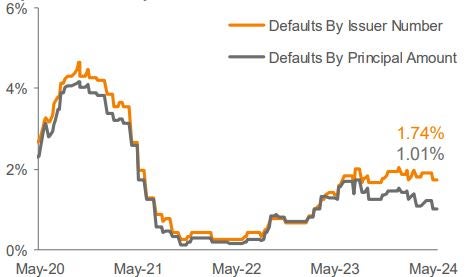

There were no defaults in the Index this week.

Source: Pitchbook Data, Inc./LCD, Morningstar ® LSTA ® Leveraged Loan Index. Additional footnotes and disclosures on back page. Past performance is no guarantee of future results. Investors cannot invest directly in the Index. *The Index’s average nominal spread calculation includes the benefit of base rate floors (where applicable).