Voya’s Multi Asset Strategies and Solutions team is committed to helping our clients and investors weather turbulent times. Here’s our latest thinking and portfolio positioning.

What happened?

On April 2, President Trump announced 10% universal tariffs on all imports except those from Mexico and Canada, with higher levies on major trading partners. The effective 19% weighted-average increase was significantly higher than market expectations and caused ripples in global securities markets.

The tariffs target broader Europe and Asia, specifically China. Markets declined further after China and the U.S. announced retaliatory increases against each other on April 8. Then, on the afternoon of April 9—the same day many of the new tariffs took effect—Trump announced a 90-day pause on certain tariffs to most countries. China, however, was an exception: its tariff was raised to 125%.

How do tariffs affect American consumers?

Tariffs raise the prices of imported goods. As such, they act like a tax on U.S. consumers—particularly for imported goods for which there are no substitutions. Tariffs are an inflation shock that broadly erodes real (inflation-adjusted) disposable income for American consumers.

The tariffs, if fully implemented, would represent the largest tax increase on the economy since the 1968 tax hike that funded the Vietnam War1.

We expect tariffs to decrease U.S. economic activity by 1% to 1.5% (as measured by gross domestic product, or GDP) and simultaneously increase inflation by a similar amount this year. Our view is informed in part by what happened following the implementation of tariffs in 2018. Non-U.S. producers raised the prices of their goods to cover the cost of tariffs—and domestic producers followed in lockstep.

In our view, the reciprocal tariffs at current rates likely will not remain in place for long; however, if they are reapplied in 90 days and persist for a prolonged period, we believe a recession is likely. While the Trump administration has officially implemented the tariffs, we expect many countries are looking to negotiate. This state of flux is causing a proper growth scare and could lead to recession as consumers buckle down on spending and businesses reduce or delay capital expenditures and hiring. There is potential to create a vicious circle without progress on negotiations.

In our view, global equity markets have priced in a large downgrade to both U.S. and global growth similar to the technical recession in 2022 when the economy experienced two quarters of negative GDP growth. A more meaningful recession with mounting job losses, waning consumption, and decreased business spending has not yet been fully priced into equity markets.

Many of the common gauges that point to equity market lows (such as the put/call ratio, percentage of stocks below 200-day moving average, and the VIX Index) are at levels that could spark a significant counter-trend rally in equities. In fact, just on April 7, we saw a 411-point intra-day move in the S&P 500 Index. This type of volatility speaks to the emotional handwringing among investors and conflicting news flow.

What we’re focusing on

We are focused on protecting the clients and investors in our shorter-term strategies who are close to retirement while still aiming to provide solid long-term returns for our investors with longer time horizons.

We are closely monitoring the functioning of markets. In our view, the tariffs in their current state cannot be maintained indefinitely without causing additional financial stress on markets.

Our portfolios have been positioned for a counter-trend rally in equities from very oversold conditions, which we saw unfold in the afternoon of April 9th given the U.S. decision to pause tariffs on most countries for 90 days.

Equities

The year-to-date sell-off in equities has been swift and violent. We have seen a significant rerating of U.S. equities, even as companies continue to deliver solid earnings. Through the drawdown, selling was broad-based. Despite the recent stock market reversal, we see additional upside as the 90-day pause suggests the administration’s desire to negotiate with our trading partners as opposed to keep tariffs in place for a prolonged period. Within equities, we continue to prefer the earnings profile of U.S. companies over the more cyclical earnings of European equities.

Fixed Income

The bond market was functioning well until this week, when bonds started moving lower in sympathy with equities. This new development, while still unfolding, could be the result of investors pricing in a stagflation (poor economic growth and high inflation) scenario. It may require support from the Federal Reserve in the form of interest rate cuts.

Economic data

Economic data over the next few months will likely not give much insight into how the economy is handling the tariffs, especially not until retail stores run down their inventory. We are already seeing a front-loading of shopping and purchases due to expected price increases. For example, auto sales in March hit their highest level since April 2021.

Employment

Weekly jobless claims data will be especially important in measuring how businesses are managing their costs against possible uncertain consumer demand.

What’s to come?

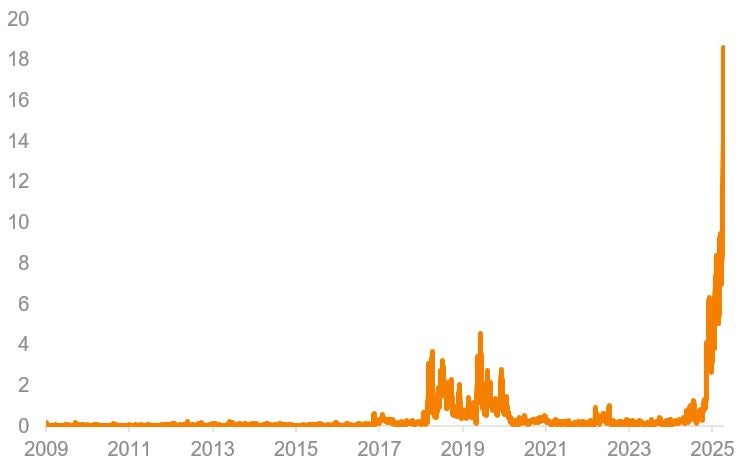

While the impact of the tariffs on financial markets is the result of a self-induced policy shock, rather than a typical growth slowdown, the news cycle can move markets quickly with global trade policy uncertainty at all-time highs (Exhibit 1).

As of 04/09/25. Source: Bloomberg Index Services Ltd.

Today’s vertical move in markets following President Trump’s announcement of a 90-day pause in tariff implementation for non-retaliating trade partners offers a glimpse at the market’s appetite for a resolution.

While the economic outlook remains cloudy, managing risk is paramount. We are continuously monitoring the situation and will make portfolio adjustments as opportunities present themselves. As always, we’ll keep our investors and clients apprised of developments as they unfold and how we are positioning our portfolios.

A note about risk: The principal risks are generally those attributable to investing in stocks, bonds, and related derivative instruments. Holdings are subject to market, issuer, and other risks, and their values may fluctuate. Market risk is the risk that securities or other instruments may decline in value due to factors affecting the securities markets or particular industries. Issuer risk is the risk that the value of a security or instrument may decline for reasons specific to the issuer, such as changes in its financial condition.