PE secondaries funds with a higher share of realized returns can offer a more durable performance profile. Unlike paper gains, realized distributions provide tangible value and fuel new compounding opportunities—key components of sustainable total return.

The connection between liquidity, cash flow, and total return

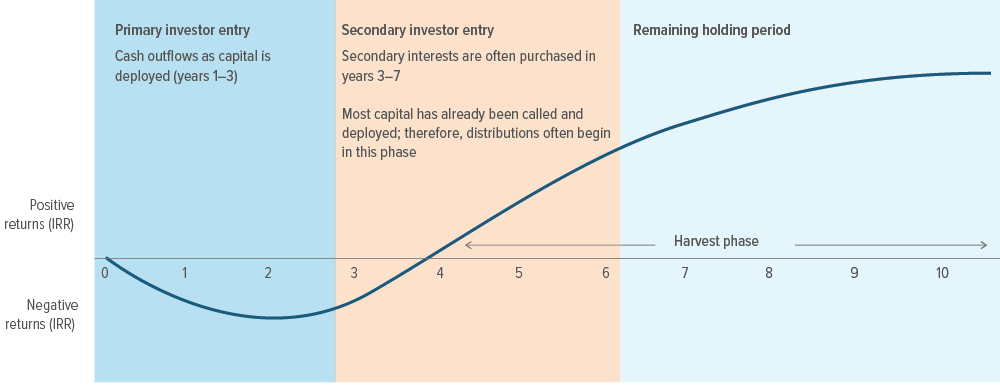

How liquidity generates cash for a fund

Liquidity is created when a primary private equity fund sells a portfolio company or receives a dividend. Once the primary fund sells an asset or receives a dividend, it distributes the proceeds to its limited partners (LPs). PE secondaries funds are LPs in a primary fund. But unlike LPs who commit capital during the early years of the fund, secondaries step in later—closer to the harvest period (Exhibit 1) — and focus on buying interests in funds with portfolios of companies that are likely to be sold soon. This means fundholders don’t have to wait as long to see cash flow, and fund managers can make more reliable projections, which helps manage risk.

Source: Pomona Capital. The above is for illustrative purposes. There is no guarantee whether expressed or implied that actual cash flow will follow this pattern. Technically, a secondary investment can occur anytime between time ‘0’ and ’10’ in this illustration. Investments in private equity involve risk, and an investor may lose some or all its investment.

How total return is calculated

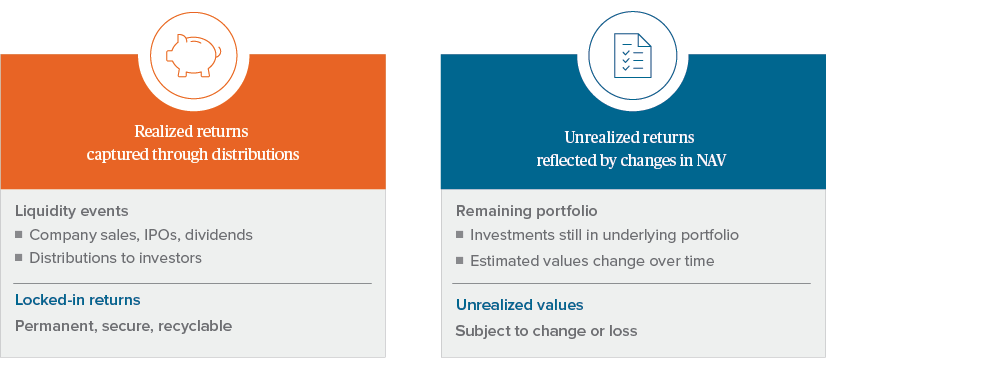

Total return includes two components (Exhibit 2):

1. Realized return: Cash distributed from investments that have been sold.

2. Unrealized return: The estimated increase in value of unsold investments, often called “paper marks” because they’re not guaranteed and can shift over time. For example, if a secondary fund buys a stake at a discount and the GP later marks it to fair market value, that creates an unrealized gain—even though no cash has changed hands.

Source: Pomona Capital.

How liquidity events fuel sustainable performance

Understanding the balance between realized and unrealized returns is key to evaluating a manager’s philosophy and the durability of a fund’s performance. Portfolios with more realized returns tend to carry lower risk, because liquidity reduces uncertainty and enables reinvestment, which should compound growth faster.

The takeaway: Portfolios that realize returns more quickly tend to carry lower risk. In the example above, Manager A was able to lock in cash gains and recycle them into fresh opportunities. Manager B continued to hold assets for longer—a riskier strategy because if the assets deteriorate and cannot be sold profitably, they consume valuable capital that could have been deployed elsewhere to earn a return. Too many “stuck” assets can cause a portfolio’s performance to suffer over time.

A note about risk:

General private equity risks: Private equity investments are subject to various risks. These risks are generally related to: (i) the ability of the manager to select and manage successful investment opportunities; (ii) the quality of the management of each company in which a private equity fund invests; (iii) the ability of a private equity fund to liquidate its investments; and (iv) general economic conditions. Private equity funds that focus on buyouts have generally been dependent on the availability of debt or equity financing to fund the acquisitions of their investments. Depending on market conditions, however, the availability of such financing may be reduced dramatically, limiting the ability of such private equity funds to obtain the required financing or reducing their expected rate of return. Securities or private equity funds, as well as the portfolio companies these funds invest in, tend to be more illiquid, and highly speculative.

Secondary investments: Risks include the ability of the manager to select and manage successful investment opportunities, the underlying fund risks, and general economic conditions. Secondaries are non-controlling investments. There is no established market for secondaries.

Primary investment: Risks include the ability to identify sufficient investment opportunities, blind pool, the manager’s ability to select and manage successful investment opportunities, the ability of a private equity fund to liquidate its investments, diversification, and general economic conditions.