Private equity investors may benefit from the value-creating initiatives seen in this hypothetical golf apparel example. In addition, secondary investors often have a potential advantage: discounted pricing, which can boost returns on invested capital.

Private equity firms are known for unlocking a company’s value using a variety of tactics, such as:

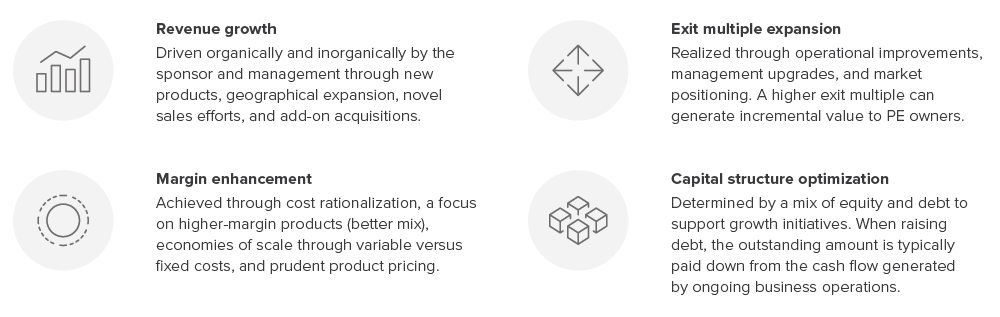

To illustrate how private equity sponsors can create value,1 consider a hypothetical investment in a golf apparel company. At the time of acquisition, the company had a value of $450 million. Over the investment period, the private equity sponsor collaborated closely with the company’s management team to implement a series of initiatives—launching new products, expanding into new geographies, diversifying the product lineup, and improving sales tactics.

These efforts yielded impressive results over the investment holding period:

- Revenue increased, adding $276 million of incremental value, which was 36% of the overall rise in value.

- The company’s EBITDA margin (earnings before interest, taxes, depreciation, and amortization) improved, contributing an additional $46 million.

- The private equity firm ultimately sold the company for an additional $145 million in multiple expansion.

- The company used cash flow from operations to reduce its debt over the life of the investment, a $298 millionvalue enhancement, which contributed 38% to the value enhancement.

As a result of the sponsor’s and management team’s efforts, the investment’s exit value rose to $1,215 million, representing 2.7x accreted value (Exhibit 1). This hypothetical case study illustrates how private equity strategies can have a transformative influence on a company’s financial performance, to the benefit of investors.

Notably, this example is based on the average accretion for the private equity industry from 1984 through 2018.1 It is not intended to represent portfolio companies held in Pomona-sponsored funds. Rather, it is an illustration of how many private equity sponsors seek to unlock value from underlying portfolio companies using a combination of similar methods—including revenue growth, margin enhancement, multiple expansion/ contraction, and changes to capital structure.

As of 01/22. Source: CAIS, Institute for Private Capital, Voya IM. Data sample includes 2,951 fully-exited deals from 1984 through 2018, with around $945 billion USD in combined equity investments and around $1.9 trillion USD in total enterprise value based on a StepStone Group proprietary dataset of private transactions. "Pre-2000" is composed of 272 deals from 1984 to 1999. "2000-2007" is composed of 1,500 deals from 2000 to 2007. "2008-2018" is composed of 1,179 deals from 2008 to 2018. The percentage represents the average portion of value enhancement attributed to each tactic. Data may not foot due to rounding. Past performance is not indicative of future results.

Potential bonus for secondaries investors: A discounted purchase price

Secondary sales are often driven by an investor’s need for liquidity. Typically, the existing fund owner sells the interest at a discount to net asset value. The average market discount over the last five years was 9%,2 potentially presenting an attractive opportunity to boost the return on invested capital.

A note about risk

General private equity risks

Private equity investments are subject to various risks. These risks are generally related to: (i) the ability of the manager to select and manage successful investment opportunities; (ii) the quality of the management of each company in which a private equity fund invests; (iii) the ability of a private equity fund to liquidate its investments; and (iv) general economic conditions. Private equity funds that focus on buyouts have generally been dependent on the availability of debt or equity financing to fund the acquisitions of their investments. Depending on market conditions, however, the availability of such financing may be reduced dramatically, limiting the ability of such private equity funds to obtain the required financing or reducing their expected rate of return. Securities or private equity funds, as well as the portfolio companies these funds invest in, tend to be more illiquid, and highly speculative.