CIO Roundtable: Historic Reform or Gathering Storm?

Chief Investment Officer

As policy uncertainty clouds the economic horizon, how much of this year’s market volatility is being driven by sentiment, and how much is declining fundamentals? Our experts take a look.

Watch Webinar Replay - Hosted by Eric Stein, Head of Investments and CIO, Fixed Income. Listen in as our investment leaders discuss market reverberations of tariffs, DOGE, geopolitics, and more.

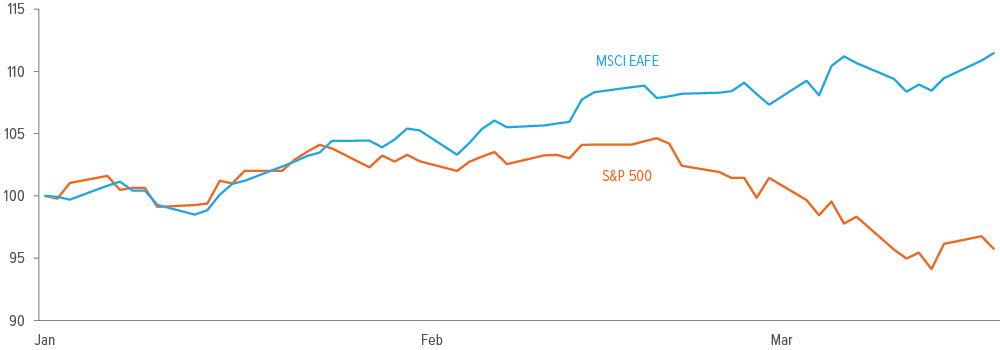

The S&P 500’s 10%+ decline from February 19 to March 13 was the seventh-fastest correction in the past century. Such market reactions are usually caused by a specific event: a banking crisis, a surprising economic report, a sovereign default. This time, it was a swift souring of optimism over aggressive policy moves by the new administration. “You can’t really watch the stock market,” said the president. And in this instance, he’s right. More important for investors is to look beyond the turbulence and consider whether the policies will ultimately strengthen the American economy—and how they are likely to affect global markets. Europe’s answer (or at least Germany’s) is a bold new fiscal determination that is fueling hopes of a new era for the Continent and attracting capital flows. Will others follow suit? In our latest investment panel, the sense of uncertainty that’s troubling markets is palpable here as well. There’s no rush to jump opportunistically into riskier assets— quality is still the play. But there are some anchoring data and key indicators to watch that may offer guidance through this adjustment period. We would love to hear what you’re thinking, too, and I look forward to continuing our conversations as the situation evolves. |

When mood swings drive markets

Eric Stein: It’s been a busy first quarter, to say the least. What’s your take on where we are in the cycle?

Barbara Reinhard: Growth looks a bit softer, and inflation data have recently plateaued after making progress. But the volatility in the first quarter has been less about economic data and more about uncertainty. The administration’s stop-and-go approach regarding tariffs, the court battles over executive orders, the upheaval in the federal system—investors don’t have a clear sense of what’s temporary and what will endure.

Fortunately, consumers aren't over-leveraged and the employment picture is still steady, so the economy can absorb a few bumps. If the chance of a recession was about 1 in 10 at the start of the year, it’s more like 1 in 4 now.

In the near term, U.S. equities look quite oversold after their peak-to-trough decline of over 10%. If headlines around DOGE and tariffs quiet down a bit over the next quarter, that could help the market find its footing.

In the near term, U.S. equities look quite oversold.

Stephen Jue: Speaking of moods, Walmart does a weekly survey of 250,000 customers to gauge how they’re feeling and what’s on their mind.1 The initial enthusiasm customers had after the election has faded significantly over the last few months. But despite worsening sentiment, customers aren’t significantly changing their spending, regardless of how the data is sliced across income levels, regions, or political affiliations. It just shows that the relationship between mood and spending behavior can be pretty loose.

Leigh Todd: There’s a phenomenon happening where the wealthiest 10% of U.S. households account for half of all consumer spending.2 That’s a lot more concentrated than in the past, which means the economy is much more dependent on this group. These consumers aren’t wallet constrained, they’re expectation constrained. If they decide to spend a little less, the economy will feel it. Plus, if the government cuts Medicaid or other federal assistance programs, lower-income cohorts could become more constrained than they already are.

Anil Katarya: In the Treasury market, 10- year yields at 4.3% have priced in some growth revisions but not a true growth scare. Credit spreads have widened from historically tight levels, but this isn’t what you’d call a dislocation. Markets are simply adjusting to uncertainty.

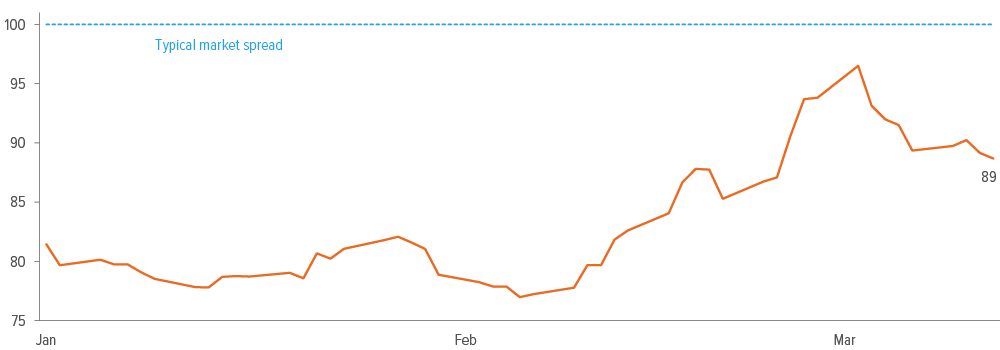

Stein: Investment grade spreads at 89 basis points (bp) aren’t exactly signaling a recession.

Katarya: Right, they’re still below a typical market level of around 100 bp. Spreads would need to widen to the 125-150 bp range before we start talking about a meaningful slowdown or a recession. The key will be first-quarter earnings. Management teams were hedging their guidance in January and February earnings calls under the guise of uncertainty. We won’t see the financial impact of some of the policy uncertainties until the end of the second quarter.

As of 03/13/25. Source: FactSet, Bloomberg, Morningstar, Voya IM.

Stein: On the equity side, growth stocks that have had phenomenal performance in recent years have been hit hard over the past month or so. Leigh, what are you seeing?

Todd: Coming into 2025, stocks were pricing in all the positive expectations of pro-growth Trump policies, such as deregulation and tax cuts, but not much of the risks. Since February, the risks of the administration’s agenda have come to the forefront. That’s put a lot of pressure on higher-growth, higher-valuation assets. But it’s not just cyclical growth at risk. Stocks with idiosyncratic secular growth stories, which tend to perform better in growth-scarce environments, have also been hit. There’s this giant sucking sound of capital flowing from the U.S. to Europe as investors latch onto the positive fiscal developments in Germany. Selling mega cap stocks has been a popular way to fund those moves.

There’s been a giant sucking sound going from the U.S. to Europe that has especially hit mega caps.

Joshua Shapiro: There’s really been no place to hide. And just when you think you'd found a safe place, the market would come in and hit that too. It’s been highly unusual, where weak spots just rotate around the market.

Jon Kaczka: Tariff issues are just such a wildcard, in terms of what gets implemented and how they’ll affect the economy. This feels to me more like a normalization than something more deeply rooted.

Stephen Jue: There are also technical factors at work. Hedge funds have been aggressively unwinding leverage, particularly in tech, media, and telecom. Earnings-day volatility is near a 15-year high, with an average move of +/-5.0% in the first quarter.3 Commodity trading advisors4 hit their S&P sell triggers in March, which unloaded a ton of supply into the market. It’s the typical “climb the stairs up and take the elevator down” situation. But it also means the worst could be behind us in this de-risking phase.

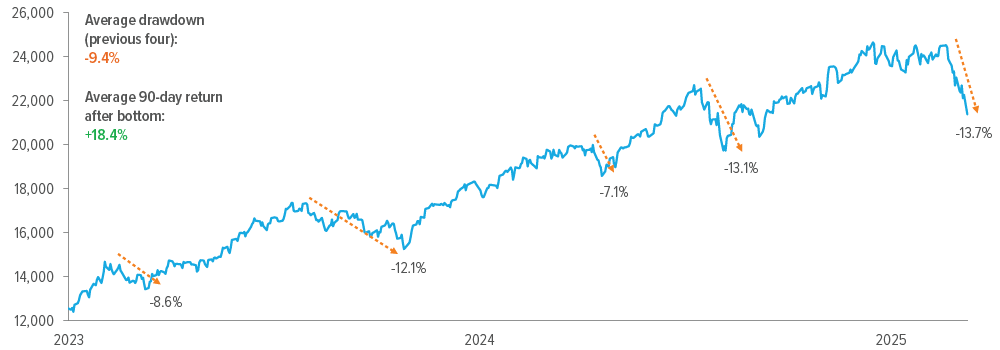

But let’s give this correction some context. The Nasdaq’s 13.7% decline through March 13 was generally in line with other drawdowns over the past few years and similar to the yen carry trade unwind last summer. Ninety days after these bottoms, the market bounced back by an average of 18%.

There’s no systemic collapse, like we had with the global financial crisis. We’re not talking about unprofitable internet ventures, like we had with the dot-com bubble. The issue today is policy uncertainty and the risk to earnings and growth outlooks if we get a self-induced economic pause. That could certainly lead to more volatility, but it looks more like a near-term leverage unwind than a break in the market.

As of 03/13/25. Source: FactSet, Bloomberg, Morningstar, Voya IM. Past performance is no guarantee of future results.

Stein: What would need to happen to start a new bull market? Not just a bounce, but a real next leg up?

Jue: First, we need clarity on tariffs. Investors need to know that the pro-growth, pro-American manufacturing agenda won’t be derailed by trade wars with allies. We need inflation readings to stay under control. February CPI’s lower-than-expected annual pace of 2.8% helped. And then we’ll need some patience until April to see how much companies revise down earnings guidance.

We’ve said that S&P earnings forecasts for 2025 had been on the high side at 17-18%. Do companies shave their numbers by 3-5%? More? If we can get through Trump’s initial shock-and-awe policy wave and start looking to tax cuts and deregulation, that could get markets back on track.

For a new bull market, we need:

1. Clarity on tariffs

2. Inflation readings to stay under control

3. Modest reductions to earnings guidance

Todd: Here’s an example with the airlines. It’s been a pretty punky year for leisure and business travel. The airlines have given plenty of excuses—it’s the flu, or it’s the weather. If we get into spring and it turns out this was just a normal seasonal slowdown rather than a real pullback in spending, that could be positive for markets.

On the secular growth side, we need evidence that AI spend is moving forward— that Amazon, Microsoft, Google, and other companies aren’t going to dramatically cut capex. We want to see movement toward developing products, agents, and apps that drive real productivity and justify continued high capex.

Jue: From the recent tech conferences I’ve attended, no one’s backing off capex at this point. There were some delays with Nvidia’s Blackwell that caused some hiccups. But DeepSeek and lower cost models haven’t reduced demand—it’s been the opposite. There’s more demand as people look to experiment with different approaches.

Tariffs hit home

Stein: We discussed in our January roundtable the importance of policy sequencing. We’ve got our answer now. But what’s the bigger driver at the moment, and are we starting to see effects in the real economy?

Reinhard: Tariffs are by far the more immediate issue. Canada and Mexico are especially vulnerable because of the amount of intermediate goods that are assembled there and sold into the U.S. With China, they've already re-sourced a lot of manufacturing in response to Trump's first round of tariffs. If these tariffs stick, it could push Mexico, and possibly Canada, into recession, and you don’t want that kind of instability on your doorstep. The administration seems to be ignoring the volatility for now. The Treasury secretary’s focus is squarely on bringing Treasury yields down to make financing the deficit more cost effective.

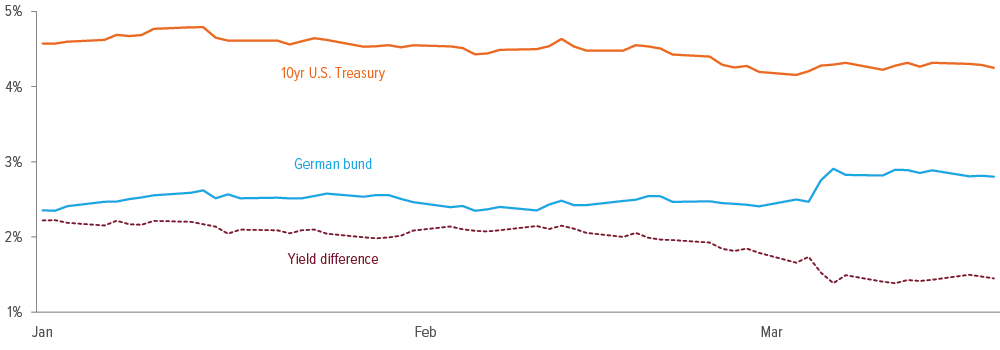

Katarya: If the goal is to push U.S. yields lower, the rise in German bund yields is making that harder. As markets react to Germany’s fiscal boom, higher bund yields will likely limit how far U.S. yields can fall, because investors now have a viable alternative for yield.

Within fixed income sectors, spreads have widened more for industries in the tariff crosshairs such as autos and manufacturers, whereas financials have performed better, as they don’t have direct tariff exposure.

Jue: You don’t want to be a business that relies on government work or cross-border supply chains. Some software companies have noted that government contracts have been paused, though it’s not clear yet whether these are temporary or permanent. Data center pure plays are more immune, especially with the continued shortages of next-generation AI systems.

You don’t want to be a business right now that relies on government work or cross-border supply chains.

Shapiro: With DOGE, there’s a transmission mechanism: There’s the direct impact of mass federal layoffs to the public sector and local economies. The first reaction is to think about Washington, D.C., but 80% of federal workers live outside the D.C. metro area—places like New Mexico, West Texas, Oklahoma, Alabama, Georgia, the Carolina coast, the Pacific Northwest.5 Granted, we’re talking a relatively small numbers of jobs compared with the overall workforce, but certain regions will feel it.

Then, like Stephen noted, there are private-sector knock-on effects from canceled contracts and funding cuts. And lastly, there’s a general uncertainty factor, which could cause broader ripple effects if worsening overall sentiment affects spending.

As of 03/19/25. Source: FactSet, Voya IM.

As of 03/07/25. Source: U.S. Department of Labor, Bloomberg, Voya IM.

Can Europe’s rally last?

Stein: Let’s circle back to Europe. The shift there has been pretty remarkable. Germany is planning a massive increase in defense and infrastructure spending to address the growing threat from Russia and doubts about American support. There’s a lot of hope that this is a fiscal sea change for the Continent. Is this a sustainable economic shift or a short-term headline?

Shapiro: I hate throwing cold water on this, because I know a lot of people see this as a watershed moment. But there needs to be follow-though. Germany may be able to get some things done quickly, but what about the rest of Europe? Creating special purpose vehicles to build up unified defense capabilities will take time and involve real implementation risks. There’s a limit to how much production European defense companies can realistically take on. And defense spending tends to have a lower fiscal multiplier. Tanks and missiles are important for security and they create jobs, but they involve limited direct consumption and high import content.

Reinhard: For the rally to continue, we need to see meaningful improvements in hard economic data such as industrial production or spending. Europe’s demographic challenges and structural issues around regulation aren’t going away. Until they get serious about applying reforms cited in the Draghi report, defense spending won’t be enough to boost long-term economic growth. I’d be skeptical about buying into this theme right now.

Until Europe gets serious about reforms in the Draghi report, defense spending won’t be enough to boost long-term growth.

Kaczka: Think of it this way. In the U.S., you have an AI capex cycle that’s durable and has productivity attached to it. In Europe, you have a new defense spending initiative after decades of underfunding, with a lot of unknowns. Just like we saw with China last September, the market likes to latch onto these aggressive fiscal spends, but details are often vague. There may be a way to invest in the Europe story down the road, but I think there will be better entry points.

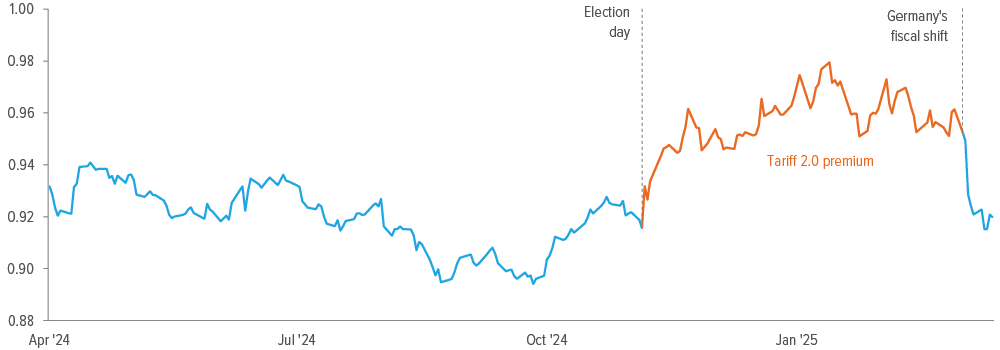

One thing to add to Anil’s point about rate differentials between Treasuries and bunds: Euro strength since January has essentially washed out the dollar’s “tariff 2.0 premium” that came on in November. Based on our analysis of currency factors, it appears that further dollar moves will depend less on tariff sentiment than on traditional currency drivers, such as relative growth and interest rates.

As of 03/18/25. Source: U.S. Department of Labor, Bloomberg, Voya IM.

As of 03/21/25. Source: U.S. Department of Labor, Bloomberg, Voya IM.

What’s your best investment idea?

Stein: Let’s close it out with your favorite idea right now. I know things can change quickly, and we’re only a few months in, but what looks interesting to you?

Reinhard: This may be broader than what you’re looking for, but I’d be adding to U.S. equities. They’ve been beaten down, and I just don’t think the economic air pocket we’re going through is going to morph into recession. A more specific idea is gold. Even though it recently cracked $3000 an ounce for the first time, the combination of geopolitical uncertainty, questions around a peace deal, and domestic policy turmoil... I think gold will be a good place to be over the next 12 months.

Todd: I'll pick a non-traditional growth area of the market and say financials. There’s been a big washout in capital market stocks like Goldman Sachs and J.P. Morgan, because M&A deal flow has been slow to develop. But deregulation is coming, and a lot of deals remain in the pipeline that need to be completed. Announcements have picked up recently, and I think the group is primed for a recovery in the back half of the year.

Katarya: I agree the financials look well positioned here. There’s no direct tariff impact, so unless we get a recession and higher credit stress, financials look pretty good. But I’d also emphasize sticking to higher-quality assets. At the moment, investors aren’t getting much value for taking risk in moving to lower-rated credits. Then, if we do get a dislocation in spreads, it puts you in a good position to take advantage of the opportunity.

Shapiro: My favorite pick at the moment is securitized credit. Spreads are some of the most compelling in fixed income at comparable risk levels, especially in segments like single-A commercial mortgage-backed securities. And U.S.-based asset pools are more insulated from geopolitical risks and trade turmoil. That seems like a pretty defensive combination for a volatile market, with enough carry to likely offset any potential credit loss.

Jue: I’d go back to the quality AI data center stocks—the Nvidias and Broadcoms, and some energy names such as Constellation Energy and GE Vernova. These are high-quality companies that have corrected pretty significantly.

Kaczka: I’m with you, Stephen. I think we’re going through more of a growth normalization than something more sinister. So I’d lean into some of the harder-hit names in large cap tech. That earnings cycle is durable, and it’s getting caught up in the tariff noise. You’ve got some of the froth out of valuation multiples, and so the risk/reward looks better.

Reinhard: Eric, what about you? What’s your favorite idea?

Stein: I kind of like duration here. I know if you look at fair value measures for Treasuries, it suggests a neutral duration posture. But with the 10-year around 4.3%, I like Treasuries as a portfolio hedge against some of these riskier assets, such as financials or growth stocks. Now, should that be limited to a U.S. Treasury trade or broaden out to bunds? That’s an interesting question. But I strongly believe there is portfolio diversification value in duration, and the low inflation reading this month is consistent with that.

Thanks for joining us today. Based on how quickly markets are moving, I just hope this isn’t obsolete by tomorrow. But I know we’ll be sending regular updates as the situation evolves.