Fixed Income Perspectives: 1H26 Themes

Head of Multi-Sector Fixed Income

As investors grapple with the potential for elevated volatility, we offer six themes we think will drive fixed income markets in the first half of the year.

We develop and regularly evaluate macroeconomic and thematic insights that drive dynamic sector allocation across our multi-sector fixed income portfolios. The following six themes reflect how we are structuring our risk profile in the first half of 2026.

1 AI ambitions meet return uncertainty

The pursuit of artificial general intelligence will continue to accelerate AI investment on an unprecedented scale, igniting a scramble for electricity, rare earth elements, and cutting-edge chips that may disrupt many dimensions of society. As money floods in, uncertainty over returns on investment and the gradual pace of adoption will spur markets to challenge valuations and capital formation.

2 The central banks’ playbook – Increased fiscal & monetary coordination

Rising interest expenses and episodic fears over debt sustainability will force central banks in developed markets to tighten coordination with fiscal policymakers. With most major central banks done with rate cuts, the Federal Reserve, stands out as it keeps trimming rates, sparking debate within the new Fed board over the true neutral rate and stoking concerns about its independence. Meanwhile, disciplined emerging market central banks are set to reap the rewards of their steady hands.

3 Momentum shifts without overheating

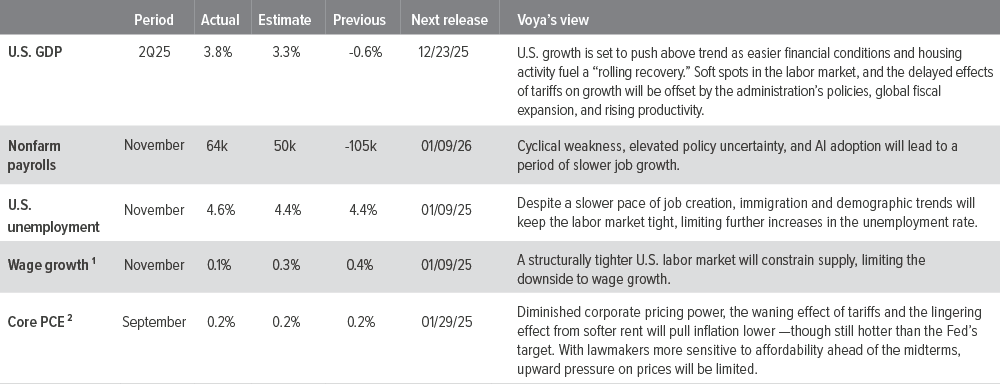

U.S. growth is set to push above trend as easier financial conditions and housing activity fuel a “rolling recovery.” Soft spots in the labor market, and the delayed effects of tariffs on growth will be offset by the administration’s policies, global fiscal expansion, and rising productivity.

4 Growth without a hiring boom

A structurally tighter US labor market will constrain supply, limiting the downside to wage growth even as elevated policy uncertainty has pushed unemployment higher. However, as growth broadens, labor conditions will stabilize, ushering in a period of “jobless growth.”

5 Inflation cooling, not cracking

Diminished corporate pricing power, the waning effect of tariffs and the lingering effect from softer rent will pull inflation lower —though still hotter than the Fed’s target. With lawmakers more sensitive to affordability ahead of the midterms, upward pressure on prices will be limited.

6 Golden age of income

Despite tight spreads, the elevated yield structure presents compelling opportunities for income generation on the front-end of the curve. A pick-up in growth will challenge the strategy of the incoming Fed chair, triggering bouts of volatility and creating attractive entry points into spread products.

As of 11/30/25. Source: Bloomberg, FactSet, Voya IM.

As of 11/30/25. Sources: Bloomberg, JP Morgan, Voya IM. See disclosures for more information about indices. Past performance is no guarantee of future results.

Sector outlooks

- Corporate earnings for 3Q25 continue to exceed expectations, with tech and financials leading the way. So far the impact from tariffs has been minimal but may flow through in the fourth quarter.

- The slowdown in primary markets has pushed spreads back to recent tights, a dynamic that should continue through year end. However in 2026, continued CapEx from tech issuers could lead to a record year for new supply.

- We continue to keep IG risk low as spreads are only slightly off historical tights. From a sector perspective, we prefer financials and utilities over industrials.

- With a few notable defaults, the market has become bifurcated, with investors showing a preference for higher quality names and lower quality names coming under pressure.

- The magnitude of uncertainty in the market backdrop favors defensive business models and balance sheets, particularly at compressed spread levels.

- Technicals are supportive but softer than earlier in the year, with cash levels down and new issuance picking up.

- The overall carry of the senior loan sector should support performance on both a total return and excess return basis.

- Fundamentals continue to exhibit stable trends, as leverage remains well inside of recent averages, while coverage ratios have bounced off recent troughs.

- The First Brands default had a real impact on the loan market, as increased scrutiny over CLO managers has led them to become more selective and avoid “cuspy” names.

- Low coupon MBS have continued to outperform, pushing spreads to relatively tight levels. However, opportunities remain in higher coupons, as well as certain CMOs.

- Declaration of a “housing emergency” could further support performance, however no definitive plans have been announced so far.

- If housing market activity picks up in 2026, new supply should follow suit.

- Uncertainty over U.S. trade policy and its spillover to global growth remains the key concern for emerging markets debt heading into the new year.

- The IMF estimates that EM growth is expected to decline slightly to 4% from 4.2% in 2025, with the moderation driven by China, India and Brazil.

- In hard currency, spreads are at historically tight levels, while local currency appears more attractive due to elevated real yields in certain countries

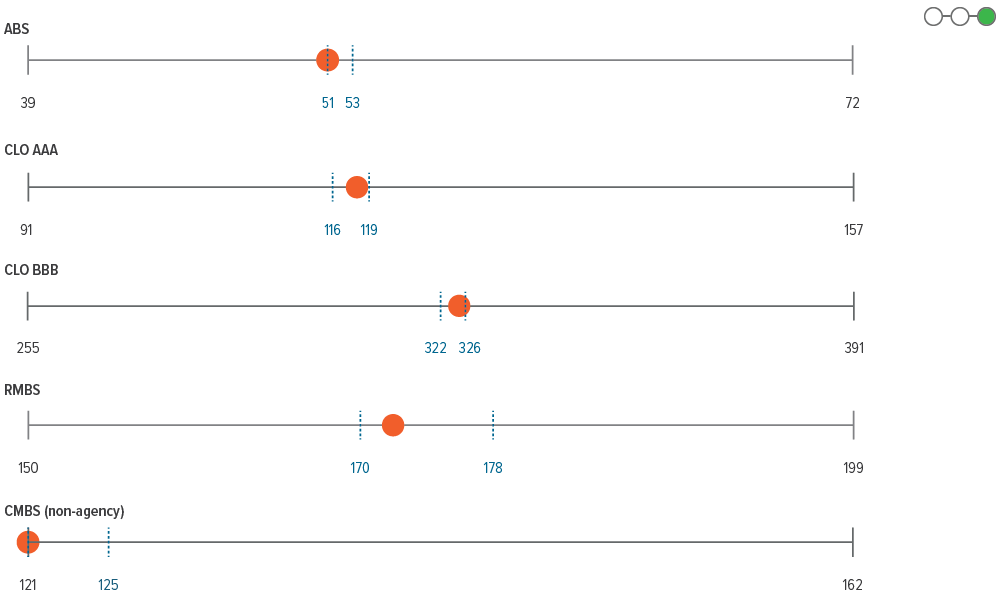

- While corporate credit spreads are starting to widen, securitized credit continues to offer attractive relative value in the current environment.

- Consumer-oriented ABS subsectors remain bifurcated, as subprime/low-income consumer cohorts are under stress, while consumer borrowing and access to credit in middle and upper income households is robust.

- CMBS is well positioned heading into year end as the new supply pipeline is considerably thinner against a backdrop of solid demand and improving fundamental outlook. That said, there are still a handful of deals that will remain under stress, regardless of the rate environment.

- Strong credit fundamentals, paired with an increase in prepayment activity, should support RMBS returns into year end.

- While investors have become more focused on credit concerns, we still view high quality CLO tranches as an attractive relative value play versus traditional corporate sectors.