Fixed Income Perspectives: Facing Fiscal Forks in the Road

Chief Investment Officer

Markets are holding steady despite mounting uncertainty, as investors, the Fed, and corporate America wait for clarity on fiscal policy and the direction of the economy.

Risk everywhere, but markets hold steady

Despite a backdrop that would normally rattle investors—geopolitical turmoil, fiscal uncertainty, and an unresolved trade landscape—risk assets have continued to grind higher. Under the surface, the market’s resilience reflects a combination of factors: labor markets remain strong, inflation appears to be contained, consumers are holding up, and capital markets are still rebounding from the steep correction in April. These dynamics have provided a floor for sentiment even as headline risks persist.

Everyone is watching the same clock

As expected, the Federal Reserve kept rates steady, and its June 18 meeting came and went with little market reaction.

Like most investors and corporate leaders, the Fed is waiting for clarity from Washington. On July 4, Treasury Secretary Scott Bessent is expected to finalize the administration’s long-anticipated tax and spending package—the so-called “big, beautiful bill.”

The proposed legislation includes a range of pro-business provisions. If those survive and tariffs are set at manageable levels, it could unlock a wave of business investment and hiring. But if talks stall or punitive trade measures take hold, low sentiment may finally translate into economic weakness. In that sense, July 4 may serve as a hinge point for the second half of the year—both for economic momentum and the Fed’s policy path.

What this means for relative value

Against this backdrop, we believe securitized credit generally offers more compelling risk-adjusted opportunities than corporate credit. Securitized sectors tend to be more insulated from the policy uncertainty dominating today’s macro environment, and several areas—particularly commercial mortgage-backed securities—remain in the early stages of recovery, offering meaningful upside potential. On the corporate side, we remain cautious toward lower-quality issuers, where signs of strain are starting to emerge. With spreads failing to fully compensate for that risk, we prefer to stay up the quality spectrum with a bias towards shorter-dated bonds.

As of 05/31/25. Source: Bloomberg, FactSet, Voya IM.

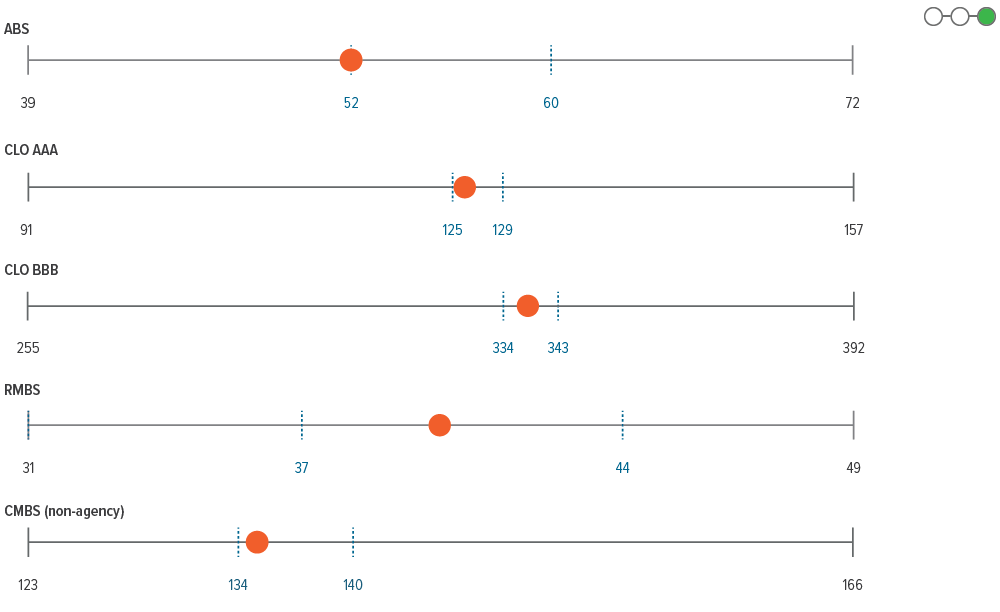

As of 05/31/25. Sources: Bloomberg, JP Morgan, Voya IM. See disclosures for more information about indices. Past performance is no guarantee of future results.

Sector outlooks

- While corporate fundamentals remain strong, we believe technicals, macroecononmic factors and valuations should have a larger impact on investment grade corporate spreads.

- With 88% of S&P 500 companies reported, 1Q25 earnings are on track for 12% EPS growth and 4% revenue growth.

- We remain underweight BBBs and favor higher quality names in this environment. From a sector perspective, we are overweight financials and utilities and underweight industrials.

- While trade policy tension has deescalated for the time being, high yield spreads are near the tights of this market cycle and risk is skewed to the downside.

- From a technical perspective, high yield fund flows remained supportive, and new issue supply continued to underwhelm.

- While corporate balance sheets entered the tariffinduced uncertainty in a solid position, businesses and consumers are likely to respond with lower spending, hiring and investment until future trade policy is more clearly defined.

- Fundamentals for senior loan issuers remain in relatively decent shape and are starting from a place of strength, particularly among higher-rated borrowers.

- We remain focused on the secondary effects of tariffs, as we are more concerned with how policy uncertainty and sentiment could affect business investment or consumer behavior.

- We expect downgrades will remain elevated in the near term given the increased concentration of lowerrated issuers in the market that are susceptible to downgrade risk.

- Despite the recent market volatility and technical moves in the mortgage space, we believe carry remains attractive.

- However, large, fast-money trades have the potential to create volatility in the near term.

- Longer-term, we believe strong fundamentals and a limited new supply backdrop should support mortgage returns going forward.

- The fiscally improved profile of the U.S. consumer is in place, although the low-income cohort is challenged. Our bias toward high-quality assets across sub-sectors remains.

- As other fixed income sectors richened over the course of May, ABS is again offering relative value on a risk adjusted basis.

- While spreads have retraced slightly, CMBS remains attractive and we continue to favor seasoned subordinate credit.

- Strong mortgage credit fundamentals and improved valuations should enable RMBS to overcome pockets of weakness emerging in the housing market.

- Weakening technicals and fundamentals make the CLO space susceptible to underperformance. We maintain a heavy bias toward high-quality managers and strong underlying collateral pools.

- Elevated real yields and softer domestic conditions suggest many EM central banks have room to continue cutting rates, but external factors may limit their flexibility.

- Absolute yield levels remain attractive relative to historical levels despite the recent rally.

- Fund flows into the sector recovered in May after the EM market experienced significant outflows in April.

Glossary of terms OAS: option-adjusted spreads ABS: asset-backed securities CMBS: commercial mortgage-backed securities RMBS: residential mortgage-backed securities CLO: collateralized-loan obligations PCE: personal consumption expenditure YTM: yield to maturity |

A note about risk: The principal risks are generally those attributable to bond investing. All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition.