Fixed Income Perspectives: Rates Finally Fall, Now What?

Chief Investment Officer

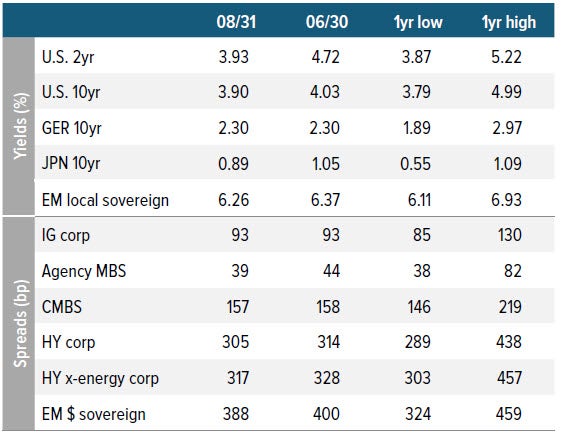

With tight spreads and a steepening yield curve, we see the most value in lower-beta spread products and high-quality securitized assets.

In a highly anticipated event, the Fed finally began easing monetary policy, announcing a 50 basis point cut in its September meeting.

While many headlines have focused on the magnitude of the first cut, it’s important for fixed income investors to take a step back and look at the Fed’s policy shift in a broader context:

The economy remains on solid footing

- The rate cut takes place at a time when the threat of a significant recession remains low (a point Chairman Powell reiterated in his statements).

- Unlike previous cycles, this period hasn’t seen a major excess buildup across industries, which typically precedes deep recessions. Instead, firms have responded to excess demand by raising prices rather than adding excess capacity, helping maintain economic stability.

- While a slowdown in GDP growth is likely—from elevated levels down to 1.5% to 2%—this moderation reflects a normalization rather than a recessionary downturn.

What does this new environment mean for fixed income investors?

- The recent steepening of the yield curve suggests that rate cuts are intended to preserve growth, as opposed to offsetting a decline. However, with credit spreads relatively tight, fixed income returns will likely stem from carry than continued spread compression.

- In an environment of tight spreads and a flat credit curve where investors aren’t getting much compensation for taking more credit risk, portfolio construction in fixed income is about optimizing the information ratio. On a risk-adjusted basis, we’re generally finding better value toward the short end of the credit curve and in high-quality securitized assets that still offer a good spread over corporates.

The bottom line: It’s a good environment for fixed income

- As the Fed shifts its policy stance amid an environment of moderate economic growth, the conditions are set for a positive, albeit measured, outlook for fixed income investors.

- The Fed’s meeting was a wakeup call for anyone hoarding high levels of cash. As we recently discussed in 3 Reasons to Get Back to Bonds After the Cash Craze, cash yields are finally poised to come down. Pivoting from cash to fixed income in the current environment offers investors the opportunity to lock in higher yields, boost return potential and gain diversification benefits.

As of 08/31/24. Sources: Bloomberg, JP Morgan, Voya IM. See disclosures for more

information about indices. Past performance is no guarantee of future results.

Sector outlooks

Investment grade corporates

- Demand for investment grade corporates remained strong despite the recent decrease in yields.

- The 2Q24 earnings season is almost complete, with results, in aggregate, exceeding analyst estimates.

- While August new issuance was higher than anticipated, we are still expecting net supply to turn negative in the fourth quarter, which should provide strong technical momentum for the sector into year end.

- From a positioning standpoint, we remain overweight financials, BBBs and the 10-year part of the curve.

High yield corporates

- The high yield market weathered the volatility in early August and produced another month of positive returns.

- While the market continues to be supported by high all-in yields, we are keeping some dry powder on hand as slowing top line growth and margin compression may provide opportunities to add risk at wider levels.

- From a positioning standpoint, we are overweight food/beverage, healthcare/pharma, energy and chemicals. We are underweight technology, as well as media/telecom companies with structurally challenged business models.

Senior loans

- Despite the early market volatility in August, the loan market remained resilient and closed out the month on a positive note.

- Strong technicals and stable fundamentals continue to support spreads, while high starting yields provide a cushion against spread widening.

- Credit selection remains key in this environment and we’re paying close attention to segments in consumer services for further evidence of continued deceleration given the lower guidance in industries such as airlines, hotels, autos, and manufacturers.

- We remain cautious of cyclical sectors and those areas of the loan market that are reliant on discretionary consumer spending.

Agency mortgages

- Overall, we expect fundamentals and technicals to support mortgage returns for the remainder of 2024.

- However, in the short term, the performance of agency mortgages will be closely correlated with overall volatility and rate directionality.

- Mortgages have recently outperformed, but spreads remain within the fair range for most cohorts.

Securitized credit

- Amid a landscape of robust securitized issuance and, on balance, supportive macroeconomic environment, the securitized credit market is demonstrating resilience, buoyed by the relative strength of U.S. consumers and initial repair in commercial real estate.

- ABS issuers are monetizing strong investor demand as the pace of new issuance has hit historically high levels. The “harmony” between issuers and investors has created a virtuous cycle of reliable primary market execution, inspiring more issuance which attracts more capital, reinforcing stable risk/ return opportunities. Crucially, underwriting quality has been strong against the later stage economic backdrop, aiding in keeping the virtuous cycle intact.

- After a long streak of outperformance, CLOs are more vulnerable to falling rates and slower economic growth, with the sector facing potentially imminent headwinds from the Fed reducing rates and the feed through into lower CLO base rates (3-month SOFR).

- Improved financial conditions have helped reduce the crisis like spread premiums once available in CMBS, effectively reducing “easy money” opportunities. As remaining problem loans continue to resolve, collateral based security selecting will slowly but surely replace simply asset allocating to the sector and “buying the sector.” In addition, the space should benefit from lower rates, especially for instruments with shorter repayment profiles that continue to trade at steep discounts.

- Residential-mortgage credit behavior is set up to remain insulated from a modest decline in home prices. Average mortgage rates for existing homeowners are <4% and the buffer of homeowners’ equity remains at or near historical highs. In our view, any spread widening inspired by potential housing weakness would constitute a buying opportunity. However, in the near-term the space will be challenged by a heavy new issuance calendar, which will offset increasing optimism for a pick-up in prepayments.

Emerging market debt

- Absolute yield levels for emerging market debt remain attractive relative to historical levels despite the recent rally.

- While China’s latest policy response appears to have stabilized the country’s economic activity, housing and private sector confidence remain weak and growth is likely to slow.

- Corporate fundamentals overall remain resilient and financial policy remains prudent. Corporate default rates are expected to be lower due to less defaults in Asia and Europe.

A note about risk

The principal risks are generally those attributable to bond investing. All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition.