Multi-Asset Perspectives: Adapting to Political Shifts and Economic Rebalancing

CIO, Multi-Asset Strategies and Solutions

Key Takeaways

Policy uncertainty drives market volatility: The Trump administration’s trade policies, including reciprocal tariffs, have caused significant market volatility and uncertainty. While tariff reductions have been announced, there may be higher levels of volatility as trade memorandums of understanding are negotiated.

U.S. equities remain resilient: Despite the fanfare international developed equities have enjoyed since the beginning of the year, U.S. equities have quietly regained their leadership. Since the April 21st double-bottom, U.S. equities have outperformed developed international equities by 5%. We think as the administration pursues more friendly macro polices, such as de-regulation and tax cuts, the U.S.’s more favorable fundamentals will drive U.S. equities higher versus their global counterparts.

Quality remains our favorite fixed income feature: We prefer higher-quality investments, especially investment grade bonds and securitized credit products, as all-in yields remain attractive. Corporate fundamentals remain favorable and as long as the US stays out of recession, corporate credit is likely to deliver value.

The current market environment offers allocators the chance to capitalize on earnings quality and an innovation cycle in large cap equities, as well as attractive yields with manageable risk and some recession protection in investment grade credit.

Tactical indicators

Economic growth (solid but slowing)

The U.S. economy, while showing signs of resilience, experienced a 0.3% contraction in 1Q25 due to a significant increase in imports as companies front-loaded purchases in anticipation of tariffs. However, underlying economic indicators, such as labor market strength, suggest the economy is healthy. We believe the probability of a recession is less than 35%.

Fundamentals (positive)

1Q25 year-over-year S&P 500 earnings growth tracking over 14% and 10 of 11 sectors growing earnings.1 Financing costs remain manageable and corporate profit margins, while off their peak, are strong by historical standards.

Valuations (negative)

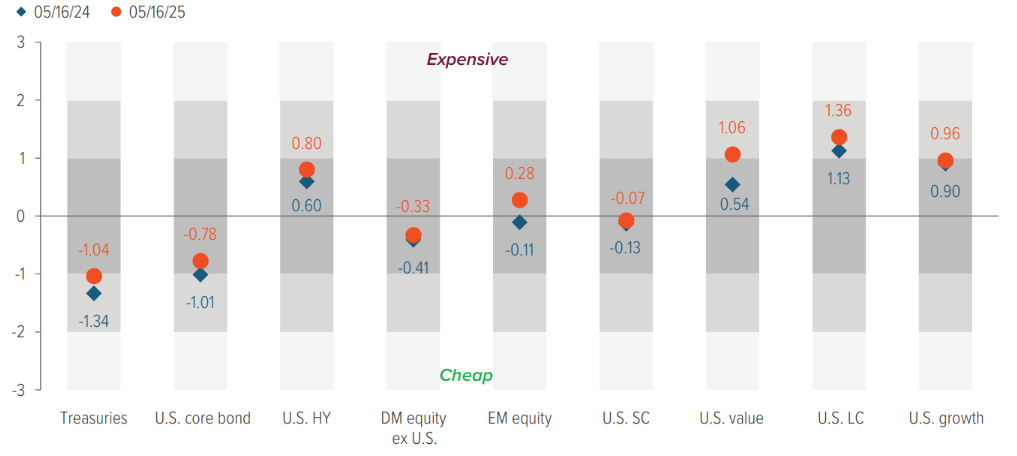

U.S. equity valuations remain relatively high, particularly for large-cap stocks. However, the quality of earnings and the innovation cycle, especially in sectors leveraged to productivity and infrastructure investment, justify these valuations. Smaller cap stocks are trading at a discount, which is justified due to weaker fundamentals and higher policy uncertainty, but they could become more attractive if sentiment improves, and the government takes concrete policy actions.

Sentiment (neutral)

Survey data, such as that from the Conference Board and the University of Michigan,2 show very poor results, yet market-based indicators have recovered.

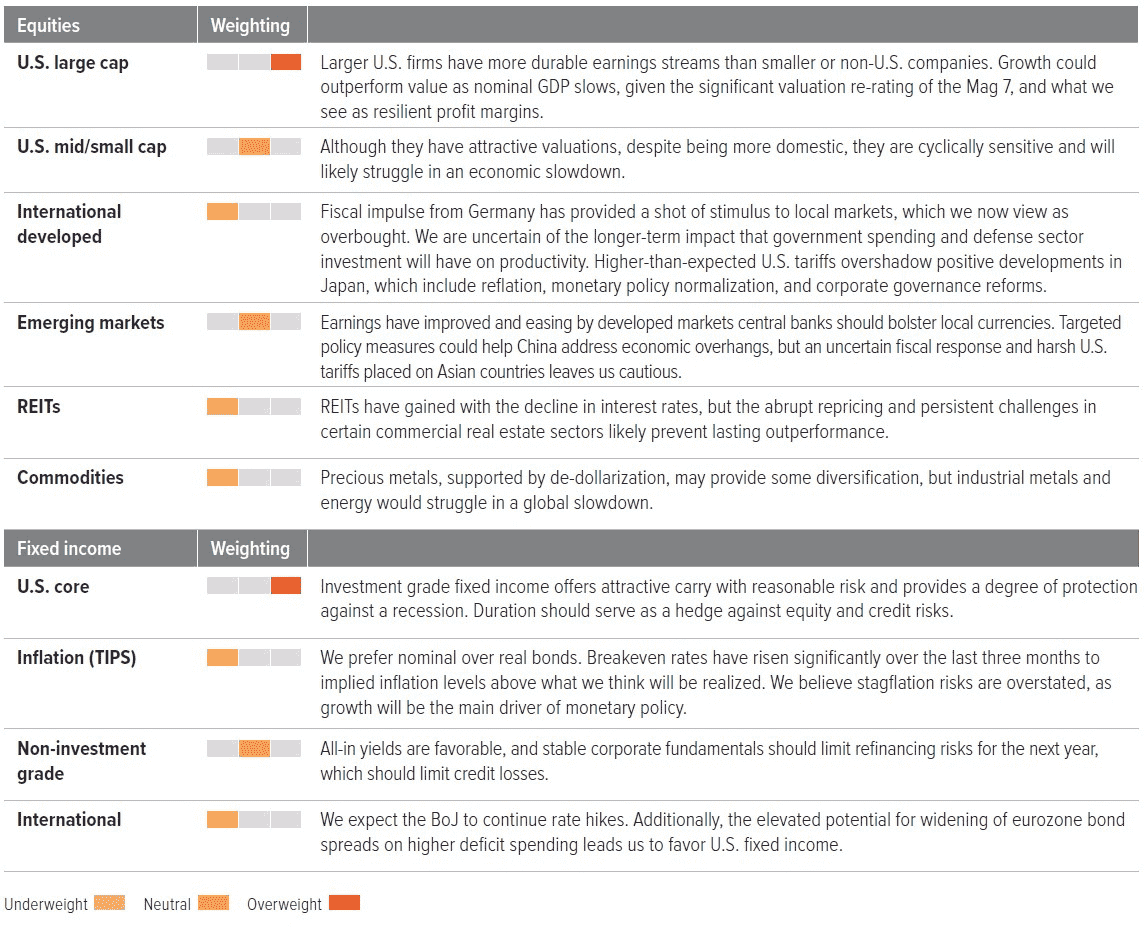

Portfolio positioning

We remain balanced between stocks and bonds, with a preference for U.S. large cap equities and high-quality fixed income.

U.S. equities: Attractive amid ambiguity

Although policy uncertainty, slowing growth, and stubborn inflation create a less stable macro environment, the U.S. economy enters a new paradigm with a solid foundation, which will help it weather this transition better than global peers. This provides a solid underpinning for U.S. equities, which we continue to favor due to expectations that they will protect profit margins despite rising input costs and deliver earnings growth over the next six to twelve months. Larger U.S. firms have more durable earnings streams than companies of other sizes or regions. While U.S. equity valuations remain relatively high (Exhibit 1), we value the country’s earnings quality and innovation cycle, particularly in sectors leveraged to productivity and infrastructure investment.

Large caps should perform well even if nominal GDP growth slows, given that Mag 7 business models are somewhat insulated against cyclical downshifts. While small caps may outperform if growth surprises to the upside, we see this as an unlikely scenario. The AI investment cycle remains intact, supported by structural demand for GPUs and cloud capacity. Even amid macro uncertainty, spending on AI infrastructure is viewed as mission critical by corporate CIOs. Furthermore, valuations of high-quality companies have repriced and could gain further with new trade deals, deregulation, or progress on tax cuts. While earnings downgrades are possible, we think the impact will be short-lived.

As of 05/16/25. Source: Bloomberg, JP Morgan, Voya IM.

International developed equities: Progress, but caution warranted

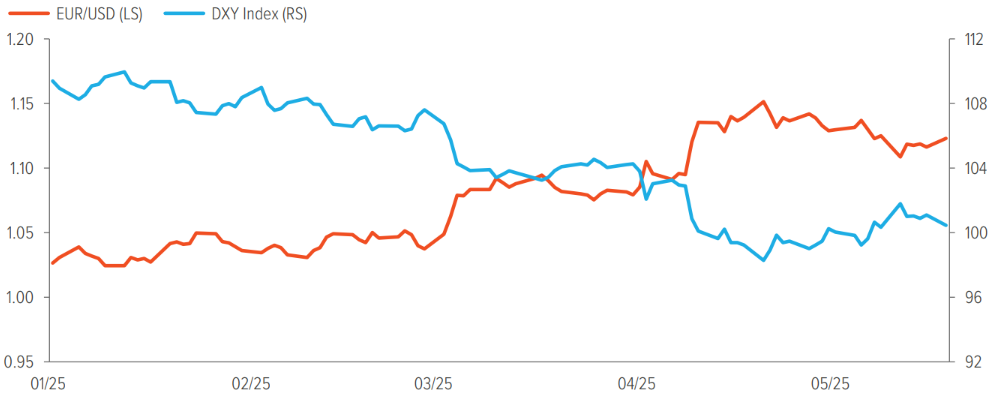

Developed international equities, led by Europe and Japan, posted strong performance year to date. Stimulus in China and looser fiscal policy in Germany—particularly a surge in defense spending—have lifted investor optimism. But sustaining momentum in Europe will require concrete improvements in industrial production, consumer activity, and capital investment. This remains difficult given that coordination of fiscal, industrial, and trade policies in the eurozone is nearly impossible. The disaggregated interests create complexity and slow legislative process, and that is unlikely to play well in the current regime marked by rapid change. While the need for improvements could catalyze Europe to come together and create the necessary reform to compete with China and the U.S., history suggests remaining skeptical until evidence shows commitment to dropping ideological differences and narrow self-interests for the broader benefit of the region. In addition, our expectation for a stronger euro (Exhibit 2) could be a headwind to exports, which are a crucial component of eurozone output.

We are neutral on Japanese equities, as supportive structural reforms are balanced by external headwinds. Japan continues to benefit from improving corporate governance, with a notable pickup in share buybacks and capital discipline. Stable domestic fundamentals, modestly growing wages, tight labor markets, and a transition from deflation to modest inflation are encouraging households and institutions to rotate into risk assets. However, the recent imposition of U.S. tariffs, particularly on autos, poses a threat to Japan’s export-heavy sectors, while a strengthening yen may further weigh on corporate earnings by reducing global competitiveness. Sluggish demand from China and other key trading partners adds to the uncertainty.

As of 05/16/25. Source: Bloomberg, JP Morgan, Voya IM.

Emerging markets: Still a tariff battleground

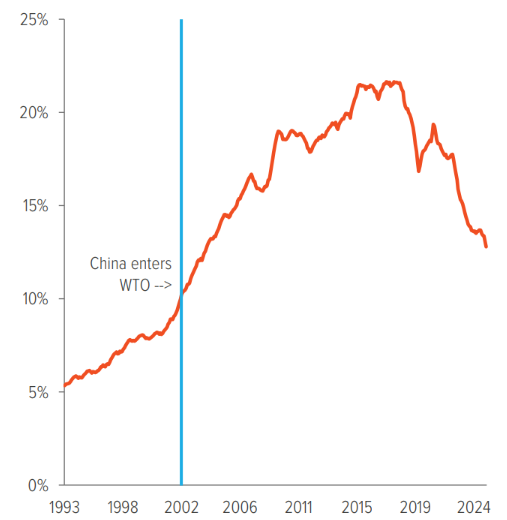

China is the primary target of the U.S.-initiated global trade war. China exports more to the U.S. than any other country and has accumulated a massive surplus that the Trump administration wants to reduce. The disintegration of U.S./China trade that began because of Trump’s first-term tariffs resulted in China agreeing to enhance intellectual property protections, reduce currency controls, and increase purchases of U.S. goods by $200 billion, which never happened. In his second term, Trump has upped the ante, causing a reconfiguration of global supply chains as China’s share of U.S. imports fell to 2004 levels (which was soon after it entered the World Trade Organization) (Exhibit 3).

Although baseline tariffs are still higher than before Trump took office, the temporary reductions in duties are welcome relief for both sides. However, the pause is only for 90 days, and nothing concrete has been decided. Given the extreme level of uncertainty, we continue to hold a negative, albeit improving, view of Chinese assets. Despite record-low interest rates and yields, credit growth is meager, its property sector remains over-leveraged, and consumer spending is weak. While we expect authorities to unveil fiscal stimulus to offset U.S. tariffs—and we were encouraged by President Xi’s recent meeting with business leaders, at which he implied the government will take a friendlier stance toward the private sector—we need to see tangible policy actions before we reconsider our overall emerging market positioning.

As of 05/20/25. Source: Bloomberg.

U.S. fixed income: Yield with resilience

Fixed income markets have become a battleground for conflicting signals. Policy-induced volatility has driven real yields sharply higher, challenging the traditional safe-haven status of Treasuries. We prefer intermediate-duration, investment grade corporates, as their overall fundamentals remain strong despite a potential slowdown. They offer decent carry without excessive duration risk. Agency RMBS and select securitized credit also look compelling, particularly as liquidity has returned to structured markets. The sturdy financial profile of the U.S. consumer, though challenged in the low-income cohort, should hold up well, as we expect inflation and rates to stay in a manageable range and growth to remain positive.

High yield corporates could see tighter spreads in the next six months if tariff tensions ease, but the risk of negative sentiment reducing activity is increasing, expanding the distribution of spread outcomes. Emerging markets (EM) present a modest growth outlook, with decent corporate fundamentals and generally prudent financial policies. However, elevated trade uncertainty limits our enthusiasm for this segment. Even though EM debt credit spreads have widened, we see more compelling opportunities within the U.S., which should benefit from pro-cyclical policies in the second half.

The dollar has weakened considerably since January, an unusual reaction during a period of market stress. This decline reflects concerns over U.S. trade policy, economic nationalism, and fiscal sustainability. While a complete loss of the dollar’s reserve status is unlikely, reduction in global trade could lessen the demand for dollar reserves and Treasuries, potentially impacting the U.S.’s ability to fund itself at low costs. The dedollarization trend, which has been ongoing since the global financial crisis, is creating opportunities for alternative investment destinations, but no clear contender has emerged to fully capitalize on the dollar’s structural weakness. Currency volatility may continue, but we expect the dollar to stabilize over the medium term as trust in the currency is gradually rebuilt, influenced by cyclical, political, and structural factors.