Key Takeaways

Macro: The impact of tariffs depends on many factors, but Trump’s campaign proposals could increase inflation by more than 2%, significantly more than the 2018 tariffs.1

Fixed income: The uncertainty surrounding tariffs and the subsequent impact on inflation may lead to a continued pause on rate cuts, supporting the “higher for longer” narrative in interest rates.

Equities: If a trade war persists, 2025 earnings growth (initially projected to be roughly 8-9%), could be slashed in half. However, companies that can absorb the higher costs, including defensive companies and some domestically focused small caps, may offer attractive opportunities.

The full impact of the announced and future tariffs remains uncertain. Aiming to mitigate risk, investors are shifting their attention toward U.S.- focused small caps and more defensive sectors, such as real estate and consumer credit.

What happened

On February 1, 2025, President Trump signed executive orders to increase tariff rates on imports from Canada, China and Mexico. Nine days later, he announced additional tariffs on imported steel and aluminum, along with retaliatory levies on countries that tax U.S. exports. While the duties on Mexico and Canada were temporarily paused, China’s went into effect. Further announcements are expected, which will likely heighten uncertainty.

Investment implications

Macroeconomy: Tariffs may cause numerous downstream impacts

Trump enacted tariffs during his first term, but the scale he hinted at during his 2024 campaign is significantly larger. Uncertainties surrounding a possible trade war include the responses of affected countries, potential price increases by companies, and the availability of substitute products. Even when tariffs are announced, they may not always be implemented. These unknowns will ratchet up market volatility.

Using 2018 as a reference, the impact of import taxes on inflation was estimated to be under 0.4%, with indirect effects (from increased input costs) roughly three times greater than direct impacts (from higher finished goods prices).2

If Trump proceeds with his proposed 60% tariff on China and 10% on the rest of the world, core inflation could rise by an estimated 1.4% to 2.2%.3 Such a significant increase in inflation could halt the Federal Reserve’s rate-cutting cycle and potentially lead to rate hikes.

Notably, even goods under $800 (which were previously exempt) may be subject to these taxes. And duty drawbacks—a loophole previously used by China—will no longer be available.

Forecasters predict that consumers will ultimately face rising prices in a trade war, which could stall economic growth. For instance, imports from Canada, China, and Mexico totaled nearly $1.4 trillion over the past 12 months, accounting for approximately 4.7% of GDP. If the additional tariffs go into effect after the 30-day stay, along with those already in place on Chinese imports, they could result in a $260 billion annual tax increase for domestic importers. If these costs are passed on to consumers, prices may rise by 0.3% to 0.6%. This could lead to a 50-70 bp increase in core personal consumption expenditures (PCE) and a 30-50 bp reduction in GDP.4

The U.S. dollar may strengthen as a result of these tariffs. However, supportive fiscal measures could mitigate the negative impacts of a tariff war. President Trump may also attempt to weaken the USD, as he did during his first-term trade war.

Stocks: Risk-off positioning may favor defensives and domestically focused names

We believe that most trade wars may be avoided or short-lived because the pain in the involved countries’ economies will be too high to bear for long. (The stay on tariffs to Canada and Mexico seem to support this view.) However, if some should last longer, the level of uncertainty and resultant supply chain issues may be much worse than in 2018. We estimate that a sustained period of tariffs could halve U.S. corporate earnings growth this year.

Voya's ViewOverall, we believe the uncertainty surrounding tariffs will lead to a risk-off positioning in the market until one of the following occurs:

But with a prolonged trade war and no fiscal support, we estimate the U.S. market could experience a peak to trough drop of 10%. Current high multiples and rising uncertainty provide very little cushion to absorb this shock. We consider each company’s fundamentals and exposures to tariffs independently. However, broadly speaking, we expect autos, some manufacturers and consumer discretionary stocks may be hardest hit. Meanwhile, certain defensive sectors—such as health care, consumer staples and telecom companies—could perform better in the long term. Some U.S. smaller caps could also outperform as their revenues are more domestically focused than those of larger peers, (but they may still feel the effects of higher prices on input costs). |

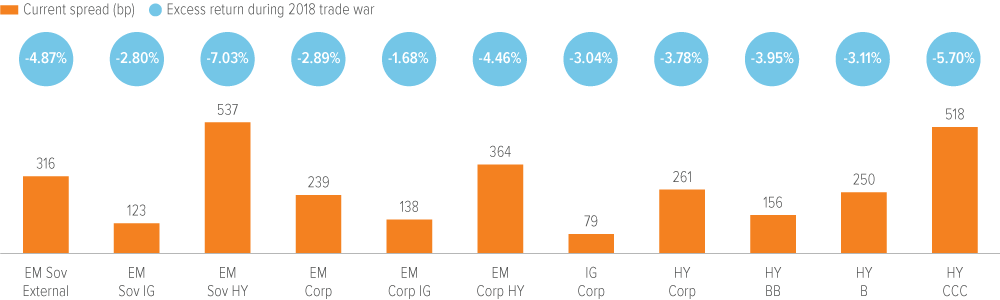

Bonds: Tariffs may delay or halt rate cuts

We believe the market had somewhat anticipated tariffs as yields rose significantly at the end of 2024. This rise was driven by better growth expectations and higher uncertainty, suggesting that even substantial actual growth or delivered uncertainty might not significantly impact yields at the moment. The muted yield reaction over the weekend further supports this view.

But, are spreads fully pricing in the potential effects of these tariffs? As a gauge, we can look at the performance in 2018. However, sell-offs occurred primarily in the fourth quarter, indicating that other factors, in addition to the trade war, likely contributed to the market’s movements that year.

Voya's ViewA prolonged trade war would further delay Fed rate cuts, impacting shorter-term yields more than longer-term yields, which may benefit from a flight to safety. Corporate credit sectors would likely be more exposed to the negative effects of a trade war because they are more dependent on international trade. With credit spreads already very tight, there is a strong bias for these spreads to widen. Meanwhile, certain domestically focused sectors, such as U.S. commercial and residential real estate and U.S. consumer credit, are more insulated from geopolitical issues, like a trade war. These sectors are less reliant on international trade and may therefore experience less direct impact. |

As of 01/31/25. Source: JP Morgan for EM spreads, Bloomberg Index Services for all other spreads. Excess return is for 2018.

A note about risk

The principal risks attributable to investing in stocks and related derivative instruments: Holdings are subject to market, issuer and other risks, and their values may fluctuate. Market risk is the risk that securities or other instruments may decline in value due to factors affecting the securities markets or particular industries. Issuer risk is the risk that the value of a security or instrument may decline for reasons specific to the issuer, such as changes in its financial condition.

The principal risks are generally those attributable to bond investing: All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition.