National Champions: Where Will the Government Invest Next?

Head of Value

SVP, Head of Responsible Investment and Thematic Research

VP, Sustainability Research Analyst

Key Takeaways

Capital is shifting: Government support is moving beyond traditional grants and contracts toward equity stakes, loans, guarantees, purchase commitments, and pricing support. That capital is increasingly directed at companies tied to national security, technology leadership, and resilient domestic supply chains.

Competition is accelerating: China’s scale in critical supply chains and advanced manufacturing is pushing U.S. policy toward a more active role in strategic sectors. Strategic technologies, defense capabilities, and critical supply chains are likely to remain focal points as the administration seeks to strengthen U.S. capacity and reduce dependence on foreign supply.

Analysis must adapt: Government support is becoming part of our broader fundamental research and portfolio construction process. We are incorporating it as a complementary factor when assessing cash flow visibility, valuation, position sizing, industry tilts, and portfolio-level risk.

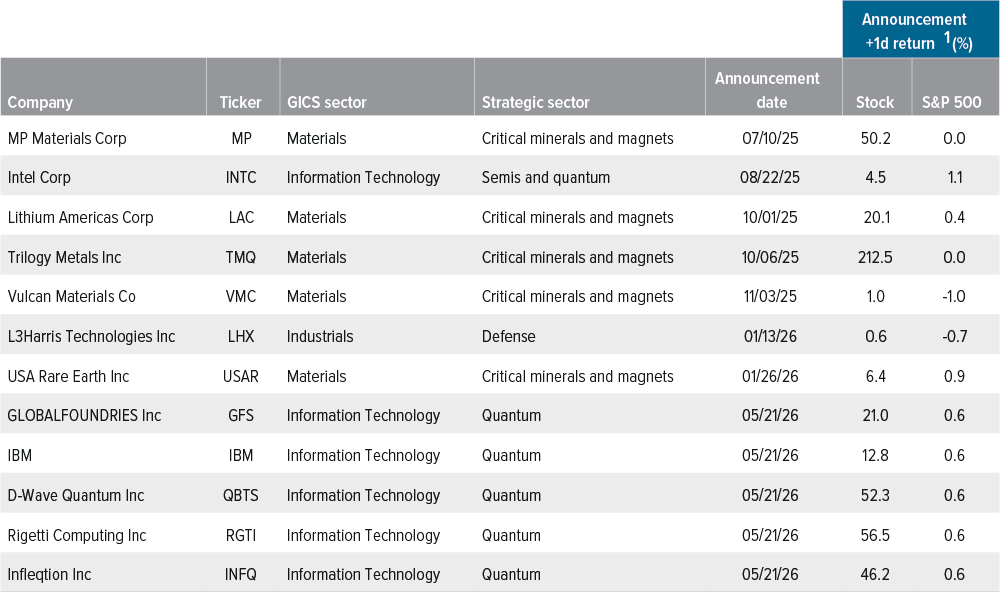

The Trump administration is taking stakes in chip, defense, quantum, and rare earth companies that align with policy priorities. These “National Champion” stocks could see long-term competitive advantages that aren’t immediately apparent.

The government is becoming a market-moving investor

Federal involvement in private enterprise is not new. U.S. presidents have long used diplomacy to support American industry. But over the last 12 months, the Trump administration has moved from advocacy to co-ownership, marking a departure from a 50-year trend of deregulation and privatization. For the first time, the government is using equity stakes to proactively shape industrial policy and protect national interests.

The terms of these investments have differed by sector, company, and funding source. Some stakes limit ownership and governance rights to protect existing shareholders. Others combine capital, purchase commitments, and pricing support to encourage domestic production in areas where private funding alone may not move fast enough.

As of 06/30/26. Source: Bloomberg, Voya IM.

1 Price return for day of announcement and the following day.

These companies are emerging as de facto “National Champions”: firms whose strategic importance may lead to policy-linked advantages that competitors lack. For example, government support can enhance access to capital through equity stakes, loans, guarantees, or warrants. It can improve demand visibility through procurement commitments, offtake agreements, or price floors. And it can validate a company’s strategic importance, which may help attract private capital over time.

In our view, National Champion status can become an important advantage if it helps a company gain share, scale faster, and strengthen its competitive position. The market may be slow to price these potential future benefits, creating a new source of potential opportunity for fundamental investors.

Strategic competition is reshaping where capital flows

Recent government investments haven’t been isolated interventions, but rather, part of a broader effort to strengthen U.S. capacity in sectors where economic leadership and national security increasingly overlap.

China’s scale is forcing a new U.S. response

The U.S.-China relationship combines deep economic ties with rising strategic competition. The pressure point is control over the technologies and inputs that may shape future economic and military strength. The United States has used export controls on advanced semiconductors, limits on investment in sensitive sectors, and restrictions on Chinese technology firms. China has used manufacturing scale and supply chain control, especially in rare earths and key minerals, to improve its position.

China’s innovation capacity has also strengthened. It now combines manufacturing scale, state policy support, and faster commercialization in strategic sectors. That shift is evident in advanced manufacturing and robotics, as well as in critical supply chains: China controls roughly 90% of active pharmaceutical ingredients and holds more than 40% share in global solar, wind, lithium-ion battery, and electric vehicle markets (Exhibits 2-3). The investment question is where the next “EV moment” will appear—and where China’s scale will prompt a targeted U.S. policy response.

Source: IEA (2026), “Global EV Outlook 2026”, IEA, Paris https://www.iea.org/reports/global-ev-outlook-2026, License: CC BY 4.0; IEA (2022), “Solar PV Global Supply Chains”, IEA, Paris https://www.iea.org/reports/solar-pv-global-supply-chains, License: CC BY 4.0; IEA (2024), “Advancing Clean Technology Manufacturing”, IEA, Paris https://www.iea.org/reports/advancing-clean-technology-manufacturing, License: CC BY 4.0; Council on Foreign Relations (05/15/26), “The U.S.-China Trade Relationship: What’s Behind the Competition?”

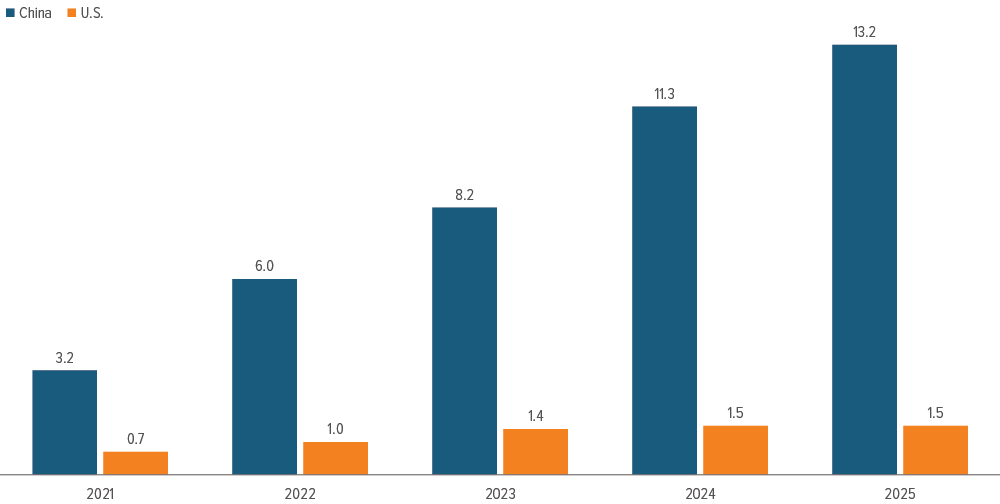

IEA (2026), Electric car sales in China, 2021-2025, IEA, Paris https://www.iea.org/data-and-statistics/charts/electric-car-sales-inchina- 2021-2025, Licence: CC BY 4.0.

Policy support is following national priorities

Against this backdrop, the administration’s policy agenda has focused on U.S. innovation, supply chain resilience, and economic independence. Those goals are translating into three investable priorities:

- Reshoring industrial capacity and manufacturing

- Advancing technological innovation

- Reinforcing national security through economic independence

This policy direction is showing up in concrete support for strategically important industries. In defense, procurement contracts and payment guarantees can accelerate weapons production. The Department of Defense also made a $1 billion convertible preferred equity investment in L3Harris Technologies’ Missile Solutions unit, which is expected to convert to common equity when the division is spun off later this year. In pharmaceuticals, where supply chain dependence and pricing are the main concerns, the administration has leaned more on trade policy, regulation, and pricing arrangements. In technology, it has used equity stakes in companies such as Intel alongside CHIPS Act funding for large semiconductor fabrication plants.

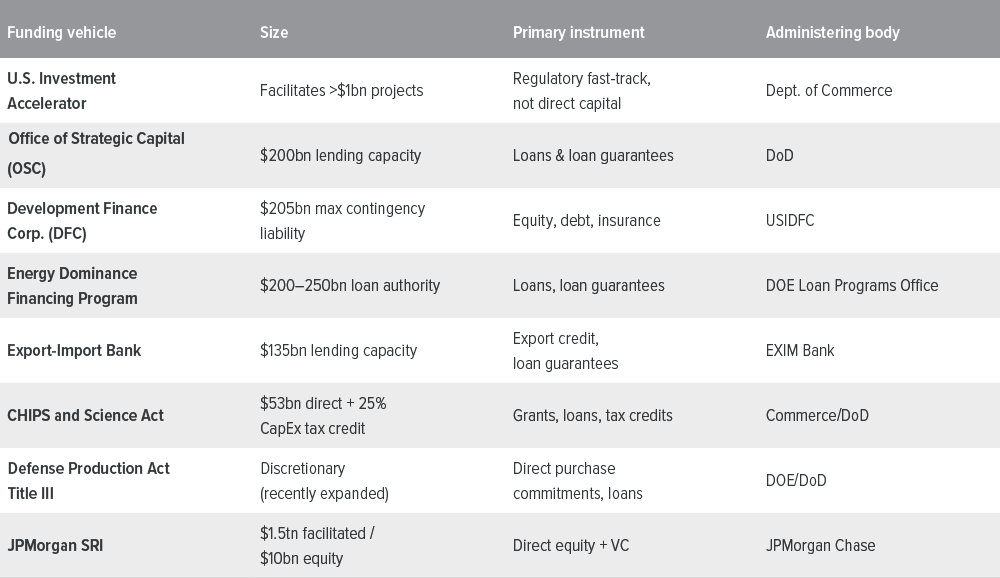

The scale of potential investment is significant, spread across multiple agencies and programs (Exhibit 4).

Source: Voya IM.

Identifying the next targets

We expect additional investment to cluster in areas where the administration’s policy agenda, national security concerns, and competition with China intersect: semiconductors, AI, defense, cybersecurity, and critical minerals. Securing mineral supply chains is already part of the policy response. The same logic applies to domestic capacity in energy, advanced manufacturing, and defense inputs.

Frontier technologies are likely to receive more attention as well, including quantum computing, advanced AI, autonomous systems, humanoid robotics, space, and cyber capabilities with both commercial and defense uses. China’s lead in robotics and battery-dependent automation may increase the likelihood of targeted U.S. efforts to build domestic competitors and limit China’s access to U.S. technology, capital, and market demand.

Narrowing the field of potential targets from sector themes to individual companies becomes trickier. But companies that have drawn attention in the past tend to share several traits:

- U.S.-domiciled businesses that offer a clear fit with stated policy goals

- Scarce, U.S.-based physical assets, such as mines or fabrication plants

- Supply chain centrality

- Prior federal funding or public support from the administration

- High capital needs and insufficient private funding to rapidly scale capacity

Importantly, these are not companies in need of bailouts. Rather, the additional support may help them to expand capacity at a pace and scale required by the country’s strategic priorities.

Strategic alignment is becoming part of our fundamental analysis

We first took note of Trump’s investment-led policy approach in aerospace about a year ago, when Trump used tariff leverage to compel more foreign purchases of U.S. aircraft. The possibility of similar support for National Champions reinforced our conviction in semiconductors and raised our interest in quantum computing. As more examples of this trend have emerged over the past 12 months, we have noted that repricing has been uneven, creating a durable entry window beyond the initial investment.

Market lag is an opportunity

Standard valuation frameworks may understate companies whose cash flows are shaped partly by policy, not purely market demand. Government co-investment also tends to unlock private capital over time. That can leave room to evaluate the announcement after the fact, assess whether policy support changes a company’s long-term outlook, and determine whether the opportunity is already reflected in the share price.

Support with strings attached

The same forces that can strengthen a company’s investment case can also introduce new risks. One risk is governance: Even minority equity stakes can introduce implicit government influence over strategic decisions, potentially misaligning management incentives and deterring private investment (illustrated by the market’s initially cautious reaction to the Intel stake). There is the risk that a future administration could have different industrial priorities or a more cautious view of government co-ownership. Government support may also increase public scrutiny or drive speculative valuation spikes.

For clients, the takeaway is not about chasing every policy announcement but recognizing that government support may become a more durable input into competitive advantage. The opportunity is to identify where policy alignment improves fundamentals, while staying disciplined about governance, valuation, and execution risk.

As strategic global competition intensifies, we believe the National Champions theme could remain relevant through Trump 2.0 and beyond, making policy alignment an important consideration in our sector positioning and company selection process.

A note about risk: The principal risks are generally those attributable to investing in stocks and related derivative instruments. Holdings are subject to market, issuer and other risks, and their values may fluctuate. Market risk is the risk that securities or other instruments may decline in value due to factors affecting the securities markets or particular industries. Issuer risk is the risk that the value of a security or instrument may decline for reasons specific to the issuer, such as changes in its financial condition.