Key Takeaways

Rising defaults and falling returns have increased redemption pressure in some retail private credit funds, though it remains unclear whether the stress is isolated or more widespread.

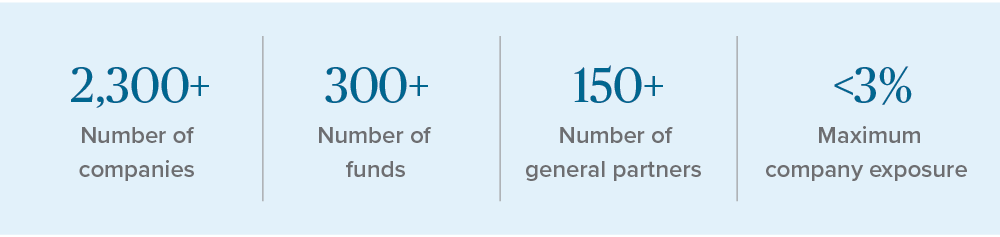

Pomona Investment Fund (PIF) is not a private credit fund; it is a private equity secondaries fund with stakes in over 2,300 companies, and as such has only limited exposure to any private credit write-downs.

The effects of distressed debt on private equity are not as directly linked as many investors assume. Those concerned about private credit may find the greater diversification of secondaries appealing.

PIF is built on quality, diversification, and selectivity. Its long-term results are the result of preparation—not prediction.

Private credit redemption pressure and default upticks are not likely to affect well-diversified secondary private equity portfolios.

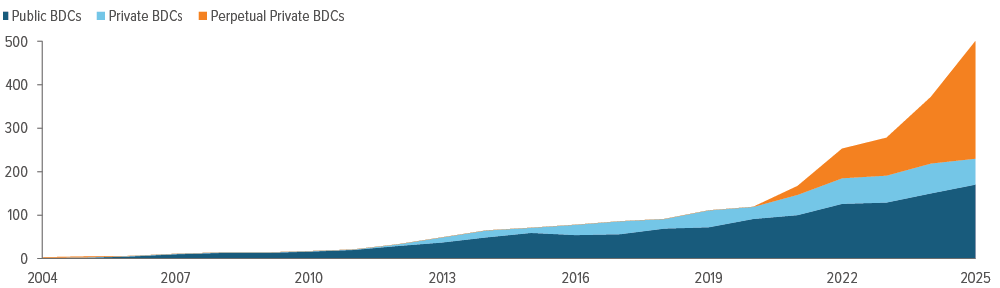

Most recently, investors have been trying to redeem their holdings in many retail-oriented non-traded perpetual private credit funds. These funds, which generally make 4-6 year speculative-grade loans to private companies, grew rapidly in recent years as rising U.S. interest rates pushed their average annual returns to 10-12% (Exhibit 1).

Late last year, investors became unsettled by several unexpected and highly publicized bankruptcies involving loans from some large private credit funds. Inflows to many of these funds began to slow. Then the launch of agentic AI in February increased anxiety around loans to software companies, which often represent more than 20% of private credit fund portfolios.1

As of 02/22/26. Source: Cliffwater; Pitchbook.

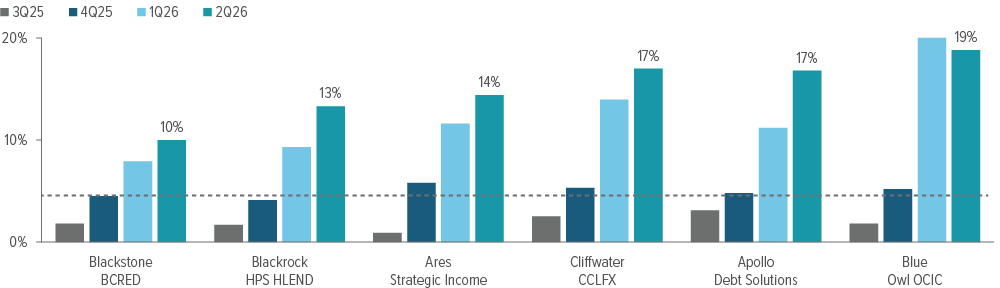

As of 07/07/26. Source: Company filings.

As with any speculative-grade lending, some borrowers will struggle and eventually default. That does not necessarily imply a systemic problem. Defaults have not become widespread, but investor concerns have contributed to higher redemption requests in many perpetual private credit funds.

These funds typically limit redemptions to 5% of NAV per quarter to avoid forced asset sales and protect remaining investors. The redemption limits are designed to manage liquidity in a disciplined, orderly manner that ensures equitable treatment for both redeeming and remaining shareholders.

But with a large number of investors wanting out at the same time, several private credit funds saw their 5% limits exceeded in early 2026 (Exhibit 2). As a result, some investors have received only partial withdrawals, fueling headlines about liquidity pressures.

Could these pressures spill over into private equity?

This is a logical question, given that estimates put “sponsored financing”— lending to PE-backed companies—at over 80% of private credit’s annual deal flow.2 And yes, debt sits above equity in the capital structure. If debt is impaired, investors may assume that equity value must also be impaired.

In practice, however, outcomes are seldom that simple. If a portfolio company is struggling with its debt, private equity sponsors have several options: They can invest more money in the company to pay off the debt; they can work with the lender to restructure the repayment terms; or they can hand the keys to the lenders and walk away—but this last option rarely happens.

In private equity, active ownership and alignment between sponsors and lenders incentivizes both parties to find solutions. The practical takeaway is that debt stress does not automatically mean the equity goes to zero.

The Pomona team has been investing through numerous cycles, and the chatter today around private credit is reminiscent of pessimism surrounding buyouts during the global financial crisis. Back then, people were claiming that as many as 50% of buyouts were likely to default on their debt.3 Actual default outcomes proved far lower than many expected—less than 3%.4 The reason: Lenders didn’t want to own and operate businesses, and sponsors had strong incentives to preserve value.

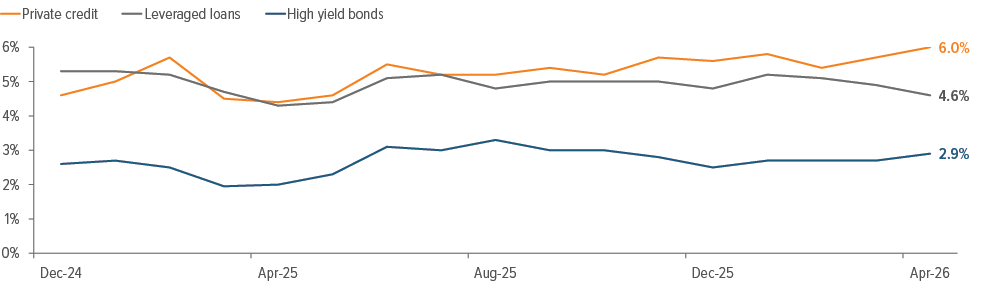

Looking at the private credit sector today, borrowers are still by and large paying their debt. While private default rates have decoupled from leveraged loans (their bank-sourced equivalent), they are not at crisis levels (Exhibit 3).

As of 06/15/26. Source: Fitch Ratings.

How will these pressures affect PIF?

PIF is not a private credit fund, nor should it be viewed as a broad bet on private markets. PIF is a highly selective secondaries fund focused on acquiring interests in high-quality private equity assets.

The fund is intentionally diversified across thousands of underlying companies in hundreds of funds (Exhibit 4). Highly selective, strategic execution is undertaken with the goal of reducing exposure to any single company, sector or manager, which in turn helps mitigate the impact of any potential credit event experienced by a portfolio company. The fund also limits exposure to high-risk market segments such as venture capital and emerging markets portfolio stakes. As a result, PIF typically executes on only 1-2% of the dollar amount of deal flow it analyzes every year. When PIF looks to acquire a private equity portfolio stake, we target underlying companies that have been in that private equity portfolio for 3-7 years.

We like to see a significant post-investment track record so we can judge whether a company is performing on their business plan and how it is handling its debt.

Ultimately, we are not in the prediction business; we are in the preparation business. Our job is not to forecast exactly how private credit, interest rates, artificial intelligence, or any other macro factor will evolve. Our job is to build diversified portfolios and evaluate whether the assets we own can withstand a range of potential outcomes.

As of 03/31/26. Source: Pomona Capital.

Is this an opportunity for secondaries investors?

Private credit stress does not automatically create opportunity for private equity secondaries. The secondary market continues to be driven primarily by institutional investors’ liquidity needs and portfolio management decisions, and broader private equity market dynamics.

Pomona’s approach remains unchanged regardless of market conditions. We identify the assets we want to own, determine the price we are willing to pay, and invest only when those conditions are met.

This has worked well so far. Our principal loss rate is less than 1% over 32 years. Those three decades encompass the dot-com crisis, the global financial crisis, the Covid pandemic, and the inflation spike in 2022.

That said, periods of uncertainty can improve buying conditions, and there are opportunities in today’s market. If we see attractive entry points for portfolios on our target list, we will seek to acquire them.

A note about risk:

General private equity risks: Private equity investments are subject to various risks. These risks are generally related to: (i) the ability of the manager to select and manage successful investment opportunities; (ii) the quality of the management of each company in which a private equity fund invests; (iii) the ability of a private equity fund to liquidate its investments; and (iv) general economic conditions. Private equity funds that focus on buyouts have generally been dependent on the availability of debt or equity financing to fund the acquisitions of their investments. Depending on market conditions, however, the availability of such financing may be reduced dramatically, limiting the ability of such private equity funds to obtain the required financing or reducing their expected rate of return. Securities or private equity funds, as well as the portfolio companies these funds invest in, tend to be more illiquid, and highly speculative.

Primary investment: Risks include the ability to identify sufficient investment opportunities, blind pool, the manager’s ability to select and manage successful investment opportunities, the ability of a private equity fund to liquidate its investments, diversification, and general economic conditions.

Secondary investments: Risks include the ability of the manager to select and manage successful investment opportunities, underlying fund risks; these are non-controlling investments, no established market for secondaries, identify sufficient investment opportunities, and general economic conditions.