CIO Roundtable: The AI Story’s Easy Phase is Over

Chief Investment Officer

Chief Investment Officer, Fixed Income

Chief Investment Officer, Equities

Senior Portfolio Manager and Equity Analyst

The first phase of the AI trade rewarded broad calls: “Buy power!” “Sell software!” The next phase will require much more discrimination across business models, capital structures, and industries.

As an investment theme, artificial intelligence is no longer just about who stands to benefit from the next wave of innovation. It’s about what markets are able to underwrite, and at what price. That shift is showing up first in places where assumptions have been most complacent. In parts of credit, software loans were often treated as if subscription revenue and enterprise value could substitute for tangible, recoverable assets. Now the market is asking harder questions. Which business models are genuinely defensible? Which cash flows are more tenuous? And what truly drives sustainable growth in a rapidly changing landscape? That, to me, is what makes this moment more interesting than the early stages of the AI trade. The easy part was identifying the theme. The harder part is understanding how it moves through markets—where it pressures credit spreads, where it reshapes earnings expectations, where it proves disinflationary, and how it changes the way investors think about the nature of “durability” itself. That’s the focus of our latest roundtable: AI as an accelerating force that may reorder how markets judge strength, weakness, and value. Thanks for joining us. Eric Stein, CFA |

Key takeaways

1. Software is the first real AI-driven stress test. The pressure showing up in software-heavy leveraged loans and private credit is an early sign of how markets may reprice business model risk.

2. Durability is the new dividing line. As AI starts to challenge routine workflows, the bigger question becomes which business models remain embedded, trusted, and hard to displace.

3. Look beyond the buildout. The next leg of the story will come from companies that are turning AI adoption into better productivity, wider margins, and stronger earnings growth.

4. AI could become its own macro force. If AI starts showing up in unit labor costs, productivity, and capital efficiency, investors may need to think differently about inflation, rates, and the business cycle.

5. Be ready for accelerating disruption. As AI reshapes business models, markets, and the broader economy, an environment of faster change and wider performance dispersion underscores the importance of fundamental research and active risk-taking.

1. Is software the first real credit fault line of the AI era?

Eric Stein: This year, the AI trade pivoted from capex and infrastructure to revenue disruption across industries, starting with software. Jim, how do you see that shift playing out?

James Lydotes: The sentiment got pretty extreme early in the year. There’s been this idea that if you were a labor-heavy business, AI should help you cut costs and improve economics. But those same companies have come under fire because the market started asking whether AI could simply replace what they do. That negativity peaked in late February, and since then the market has become more business specific. It’s now less “Which sector is dead?” and more “Which companies are actually going to leverage AI better?”

Stein: Stephen, why did software become the first real battleground? Why did this move so quickly from enthusiasm to fear?

Stephen Jue: Because the market suddenly saw a real step-change improvement in AI model capabilities. When Claude Code came out, investors started to see that these models weren’t just providing broad answers. They were writing code, moving into knowledge work, and handling specific tasks inside real business processes. That created a cascading question: Which workflows are actually defensible, and which are more replicable than we thought? The market took a shoot-first, ask-questions-later approach, especially in software. And to some extent that was understandable, as on the surface many software companies appear to be built around more routine, low-moat task automation.

The other thing that changed is that long-term assumptions stopped looking quite as solid. A lot of software companies had been valued on the idea that subscription models were durable and that there was a long runway of terminal value. Now that’s being questioned. If AI can replicate some of that functionality directly, or let customers do more on their own, the market has to reassess what those cash flows really look like five or ten years from now.

Stein: Jeff, what are you seeing from the fixed income side? Software seems to be where the stress of AI displacement is showing up most clearly, especially lower in the capital structure.

Jeffrey Hobbs: It’s really a multi-layered theme in fixed income. Software makes up just 3% of the public high yield market, but that’s where a lot of the weakness has been concentrated.1 It gets bigger as you move into other parts of leveraged credit—about 13% of the leveraged loan market and 23% of below investment grade direct lending. That’s why so much of the pressure in private credit ties back to software exposure, and business development corporations (BDCs) are a public market proxy for that. Investors are trying to reposition ahead of potential defaults on software-related debt.

Stein: Given the size of that exposure, what’s the risk that it spills into broader credit markets?

Hobbs: Historically, where you see debt growth, you tend to see debt problems. A lot of the software debt under pressure today was issued in a very different lending environment, when high enterprise multiples supported a lot of leverage. As those business models have started to look less secure, it’s become a real issue. I don’t think it’s an imminent systemic crisis, but it is big enough to have broader credit implications if spreads widen, if issuance softens, or if credit losses start to reduce investor appetite for private credit.

Stein: The Voya private credit team has approached this risk differently from some managers who are now scrambling to reassess their software exposure. What’s been the difference?

Hobbs: A big part of it is that we didn’t build portfolios assuming software credit would always behave like durable, well-secured lending. Our approach has been to stay selective and structurally insulated from areas where those risks are hardest to underwrite. We have zero software exposure in our high-yield private credit portfolio and only 2% technology exposure in our IG private credit portfolio.2

2. Which business models are vulnerable, and which still have defensible moats?

Stein: It’s one thing to say software is under pressure. It’s another to ask what’s actually vulnerable and what still has a moat. Stephen, where do you draw that line?

Jue: I’d start with the nature of the workflow. The most sensitive businesses are the ones where the work is more routine or data-entry oriented, such as entry-level coding, customer service, and some narrow point solutions. But I think the market may still be underappreciating businesses that solve harder problems, sit inside more complex workflows, and have access to proprietary data that can’t easily be disaggregated. Those companies are in a different category from businesses whose functionality is easier to replicate.

Stein: And if you’re one of those software companies trying to defend yourself, what does “fighting back” actually look like?

Jue: A lot of them are trying to infuse generative AI and agent capabilities into their products, but the challenge is that the business model is changing at the same time. Software is moving from a seat-based subscription model toward something more consumption or token based. That pushes costs up because compute becomes much more expensive when you have AI agents constantly running in the background.

And customers are still experimenting. They’re asking: Can I do this myself, can I build it myself, or is your platform good enough that I should keep paying for it? The next year or two are going to be a real transition period. Companies have to show they can integrate AI, keep customers engaged, and get to a pricing model that reflects actual value delivered. Longer term, I think it moves toward value-based pricing, but getting there is going to be messy.

Stein: It’s a double-edged sword for software on both the cost and the revenue side. Costs can rise because companies have to compete in a more compute-intensive, agent-driven world. And revenue can come under pressure because chief technology officers are trying to control tech sprawl and prevent every vendor from raising prices each year. There needs to be at least a pause in software pricing power if corporate customers think they can do some of this better on their own.

Lydotes: I’d add one more thing: Trust matters more than people sometimes acknowledge. Intuit is a good example. Earlier this year, the stock got hit because the market started assuming customers wouldn’t need TurboTax if they could just upload their W-2s into Gemini and do the work themselves. Then Intuit announced it was integrating Anthropic’s tools, and the stock rebounded.

That told you something important. If a trusted platform can show that it’s incorporating AI in a way that reinforces convenience and reliability, the existential risk looks very different. For certain kinds of software, especially where you’re dealing with sensitive personal or financial information, the customer relationship still matters a great deal.

Stein: That’s also one reason I think wealth management is such an interesting test case. AI can absolutely save costs in the middle and back office. But whether people trust something like “Wealth by ChatGPT” instead of talking to a human advisor may be much more of a generational question. That trust layer may be a moat in its own right.

3. Beyond the obvious AI winners, where else could earnings benefit in 2026?

Stein: If the first part of this story is disruption, the next part has to be about where the AI story is expanding. Stephen, where do you see the market moving?

Jue: It’s been broadening out beyond picks-and-shovels infrastructure into memory, storage, and networking. Data centers are getting bigger, more power constrained, and more distributed, so the connective tissue matters more too. That whole infrastructure ecosystem is still important.

The next leg is about adopters—the companies outside technology that can use all of that investment to drive better margins, lower costs, and higher productivity. That shift was starting to happen before the disruption trade took over. We’ve approached it with a barbell strategy in thematic equity funds: meaningful exposure to infrastructure, because the investment need is still underestimated, but also exposure to the beneficiaries in various industries that can monetize these capabilities.

Lydotes: One thing I like in that second wave is the idea that AI can help reallocate skilled time to higher-value work. Look at health care. Doctors are using AI in appointments to document and take notes. That frees up a scarce and expensive professional to spend more time on actual care. It’s the kind of use case that broadens the beneficiary set, because the gain isn’t just about reducing labor costs. It’s better use of skilled human capital.

Jue: Exactly. Industries with high labor costs and lots of inefficiencies are where this starts to get interesting. Even modest gains in efficiency can drive a meaningful boost to margins in areas such as health care, transportation, and industrials. It’s still early, but if you get a cyclical upturn, some policy support, and a few rate cuts, you could see a late-cycle economy extended by this productivity and investment wave.

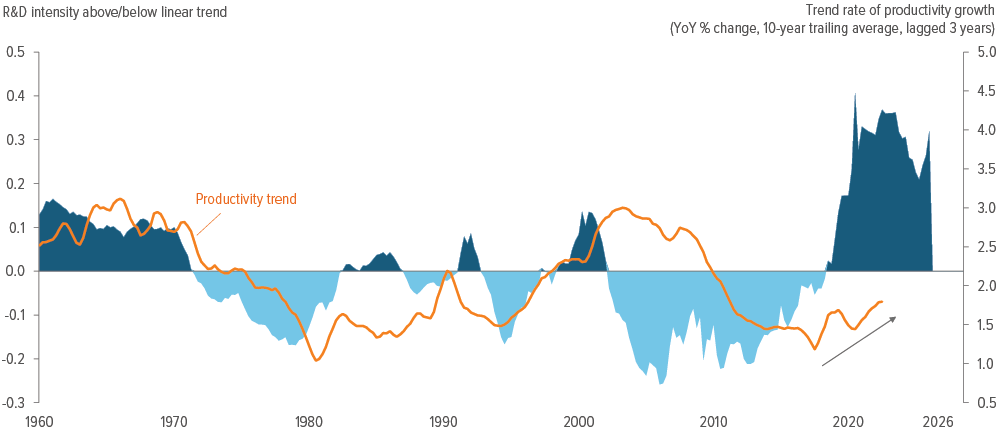

As of 03/31/26. Source: Bureau of Economic Analysis, William Blair Equity Research.

Hobbs: From the fixed income side, the infrastructure story is showing up more in the IG space. Technology is currently about 10% of outstanding IG credit, but it could represent 20-25% of new issuance this year.3 It’s part of the reason credit curves have been steepening as long-duration supply comes to market. So, even as equities start to look for second-wave beneficiaries, the original buildout phase is still very much alive in credit markets.

4. When does AI start to impact the macro story?

Stein: Before the latest geopolitical worries took over, the market was spending a lot of time on the idea that AI could be structurally disinflationary. Jeff, is that showing up in the data?

Hobbs: AI disinflation is already here, but it’s not the dominant force in the data yet. We still have other inflation pressures in the system, and in the near term, the macro backdrop still reflects those countervailing forces. But over time, it’s hard to imagine AI not putting downward pressure on labor costs and services inflation. That means the disinflationary effects have longer legs than some of the more immediate energy-related inflation shocks the market is focused on. And if that’s right, it has implications for rates and for portfolio construction. In a world where you have an inflation/disinflation tug of war, duration can start to matter differently.

Stein: So what should the market actually watch?

Hobbs: To me, it starts with unit labor costs. That’s the cleanest place to look for AI-driven productivity gains to show up. The labor market is a complicated system, so it’s hard to isolate AI in real time at a macro level. But if productivity improves and labor cost pressure starts to ease, unit labor costs are where I’d expect that to come through first.

Source: Bloomberg, Evercore ISI.

Stein: Jim, you’ve made the point that the market may be too focused on labor.

Lydotes: It makes sense to talk about labor, but one part of the story that’s under the radar is capital disinflation. If AI increases utilization across systems, you need less physical capital to produce the same output. There’s a parallel in railroads. In the 1990s, Hunter Harrison vastly improved the efficiency of the U.S. rail system, which meant they needed fewer railcars. The same thing can happen across industries. If hospitals run more efficiently, maybe they need fewer MRI machines. If farms run more efficiently, maybe they need fewer tractors. Cars are the most obvious example. Most of them sit idle almost all day. If AI makes transportation systems smarter and more efficient, you may not need as many physical assets.

Stein: So if you combine Waymo, Uber, and a really good AI algorithm, cars could optimize themselves and move around as needed. And then you’d need a lot less of them.

Jue: I also think we’re at the front end of a real productivity cycle. It’s not fully visible yet, but when I look at history, this feels more like a larger-scale version of the technological productivity wave in the ’80s and ’90s than the post-financial-crisis period. As these AI models and capabilities improve over the next five years, we could see a much stronger productivity boom than people currently expect.

That matters for the macro mix. You could end up with higher GDP growth, better margins, and less wage inflation pressure than you would normally associate with a hotter economy. The labor effects won’t be uniform. Blue-collar services may still see higher wages, while white-collar knowledge work feels more compression. But the overall picture could still be a more productive, less inflationary growth regime.

Stein: That’s what makes the labor question more nuanced than simply an “AI replaces white-collar work” story. AI is also an augmentation tool for the trades. A plumber, electrician, or contractor may not be replaceable in the same way, but they can absolutely become more productive if AI helps with routing, diagnosis, scheduling, and administrative work.

Lydotes: AI can also democratize some of the easier tasks. I recently snapped a picture of my thermostat with Gemini and it walked me through how to fix it. That would have been a low-value service call before AI. So even in areas where AI mostly augments rather than replaces, it can still change the ladder of work underneath.

5. What does it all mean in practical terms for investors?

Stein: Let me end with the longer horizon, but in a way that’s practical for investors now. What should investors actually keep in mind, both about where this ultimately takes us and about how to navigate it today?

Jue: I’d keep two things in mind. First, I still think the hyperscaler capex story is more durable than the market sometimes gives it credit for. There’s a lot of anxiety around the spending, but I do think they’re seeing returns on it, and I do think it’s strategic to their business models. If corporate AI adoption continues and all of us are using agentic AI across more business processes, that should continue to support demand for compute.

Second, I think the opportunity set is broadening. It’s not just picks and shovels anymore. It’s the companies that can use AI to improve margins, productivity, and growth. At the same time, disruption risk is going to intensify. The models are going to improve exponentially. We’ve unleashed the genie, and now we’re going to keep climbing this wall of worry about how business models evolve.

Hobbs: The uncertainty surrounding private credit and software loans is creating openings for bottom-up security selectors to pick good credits at more attractive valuations. When you look at how public and private markets continue to converge, I think these types of opportunities could show up more often heading into the later stages of the AI capex buildout.

More immediately, with markets reacting to near-term inflation risks tied to the conflict with Iran, longer durations look attractive here. That increases if AI becomes a persistent disinflationary force. The portfolio implications would be much broader than one trade or one sector—it would change how investors think about inflation regimes, rates, and duration.

Lydotes: My practical takeaway is that the easy phase is over. Over the last year and a half, you could make broad generalizations and mostly be right—all software gets hit, all power works, that kind of thing. Now we’re in the harder phase, where you have to understand how individual companies are adapting to this reality. There’s going to be much more differentiation within industries, both in operating performance and in stock performance.

Longer term, I do think the productivity story is going to play out, and it’s going to be disruptive. But I also think investors should be careful about simply extrapolating today’s bottlenecks forever. Power is the best example. AI itself should help improve energy efficiency, compute efficiency, and even grid efficiency over time. So, to me, the longer-run story is broader than labor disruption. It’s a system-wide efficiency story, which makes simplistic conclusions harder to trust.

Stein: That may be the cleanest way to frame it. The first phase of the AI trade rewarded broad calls. This next phase is going to require much more discrimination across business models, capital structures, and industries. I’d say prepare for a world that continues to disrupt itself. The disruption cycle is going to keep moving faster and faster. Think that a year ago, we had the DeepSeek moment, and people were saying U.S. AI might get pushed aside. Now we’ve moved on to the next set of questions. That cycle is just going to continue.

Lydotes: It’s simultaneously the scariest and the most exciting time to be alive.