Fixed Income Perspectives: Themes for the Second Half of 2026

Head of Multi-Sector Fixed Income

The back half of 2026 may hinge on six themes: AI spending, uneven growth, labor supply, sticky inflation, uneasy central banks, and volatile bond markets.

1 The AI supercycle is both a growth engine and a policy flashpoint.

The AI buildout looks set to keep going through the back half of 2026, with capital spending still firm and the market still willing to give companies time to prove the case. But that patience will not last forever. Investors will start asking harder questions if spending slows, productivity gains stay thin, or revenue and profit fail to follow. Regulation and politics could become the bigger swing factor, which leaves growth expectations intact for now but raises the odds of sharper repricing if the story starts to crack.

2 U.S. growth firms even as consumer exhaustion sets in.

The U.S. still appears better positioned than much of the world, with AI investment, fiscal spending, and generational wealth transfer helping keep growth near trend. The weak link is the consumer. Real income pressure could limit how much farther spending can carry the expansion, while overseas growth may run softer as higher commodity prices offset the effect of stimulus and defense outlays. That split favors markets tied to U.S. resilience, but it also leaves less room for disappointment in sectors priced for a stronger global backdrop.

3 Labor stabilizes but remains structurally tight.

Payroll growth will stabilize as tariff uncertainty and fears around AI-related job loss start to fade. Even so, labor supply remains constrained by demographics and tighter immigration policy, which should limit downside wage pressure even if hiring slows. The result may be a labor market that feels calmer without becoming soft, with bigger differences across industries. That keeps the inflation picture messy and makes it harder to predict the next move from the Federal Reserve.

4 For U.S. inflation, 3% is the new 2%.

Inflation may avoid another breakout, but it’s also unlikely to return to the Fed’s 2% target anytime soon. Recurring supply shocks in a more fragmented global economy, along with persistent demand from price insensitive AI spending and upperincome consumers, could keep it hovering near 3%. Offsets from shelter, wage dynamics, and the fading effect of tariff-related price increases should help keep it from moving much higher. That argues for a market where yields stay elevated, and duration still needs to be handled with care.

5 Central banks more tolerant but inspire less certainty.

The Fed may be willing to sit with inflation running somewhat above target if it sees the pressure as commodity-led and wage growth as contained. Even then, the policy picture may not feel settled as differences inside the FOMC complicate the policy narrative. Meanwhile other developed-market central banks with narrower mandates will likely manage a shallower hiking cycle. Rising debt burdens and fears of sustainability are also pushing central banks across developed markets toward closer coordination between monetary and fiscal policy. That leaves rates markets more exposed to policy friction, headline risk, and sudden changes in tone than a calm policy backdrop would suggest.

6 Income is back, but so is volatility.

Higher yields still offer real income in fixed income markets, which changes the starting point for investors in a good way. The catch is that spreads remain tight, leaving less cushion if growth stumbles or policy mistakes pile up. At the same time, AI spending tied to energy, defense, and supplychain self-sufficiency could still lift earnings while also planting the seeds for excess and poor capital allocation in parts of the market. That makes broad exposure less forgiving and puts more weight on sector choices and security selection across public and private markets.

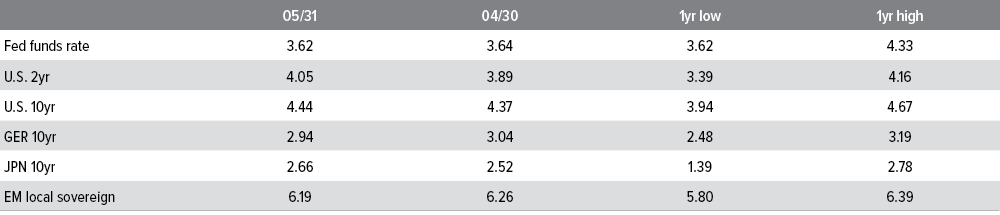

As of 06/24/26. Source: Bloomberg, FactSet, Voya IM.

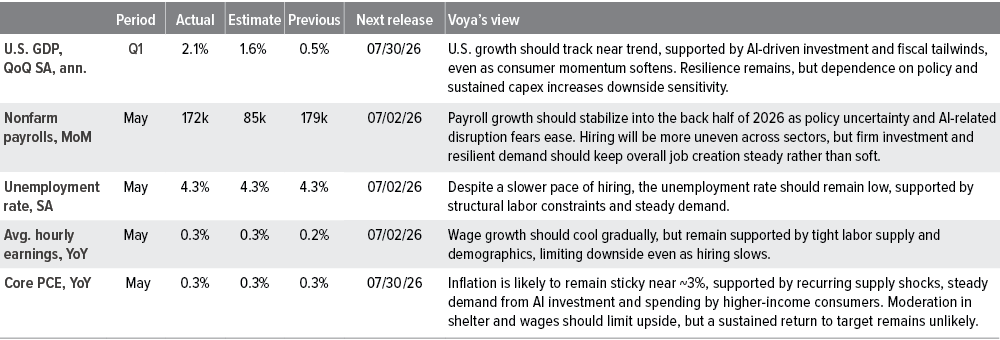

As of 05/31/26. Sources: Bloomberg, J.P. Morgan, Factset, Voya IM. SA: Seasonally adjusted. PCE: Personal consumption expenditures.

Sector outlooks

- IG spreads are back near year-to-date and multidecade tights after grinding tighter in May. Valuation (not fundamentals) remains the main constraint on adding broad risk.

- Demand remains supported by higher all-in yields, especially out the curve, while May supply was heavy but manageable and fund flows rebounded.

- Fundamentals remain strong, but rate volatility, geopolitical risk, and inflation surprises could quickly undermine tight spreads.

- High yield fundamentals and technicals remain supportive, although we see limited opportunity with average spreads hovering near all-time tights, leaving carry as the primary driver of total returns.

- We believe downside risk remains manageable, with defaults expected to remain low against a favorable earnings backdrop. However, we note increased dispersion across lower-quality and more cyclical credits.

- Positioning should favor durable business models and higher-quality BB/B risk while remaining selective in CCCs and cyclicals.

- Senior loans remain supported by strong demand technicals, especially collateralized loan obligation (CLO) formation and recovering retail inflows, even as issuer dispersion stays elevated.

- Fundamentals are stable overall, with leverage and coverage still reasonable, but liability management exercises (LMEs) and downgrade risk remain concentrated in weaker low-B issuers.

- Security selection remains critical as AI disruption, geopolitical risk, and consumer-sensitive sectors drive performance dispersion.

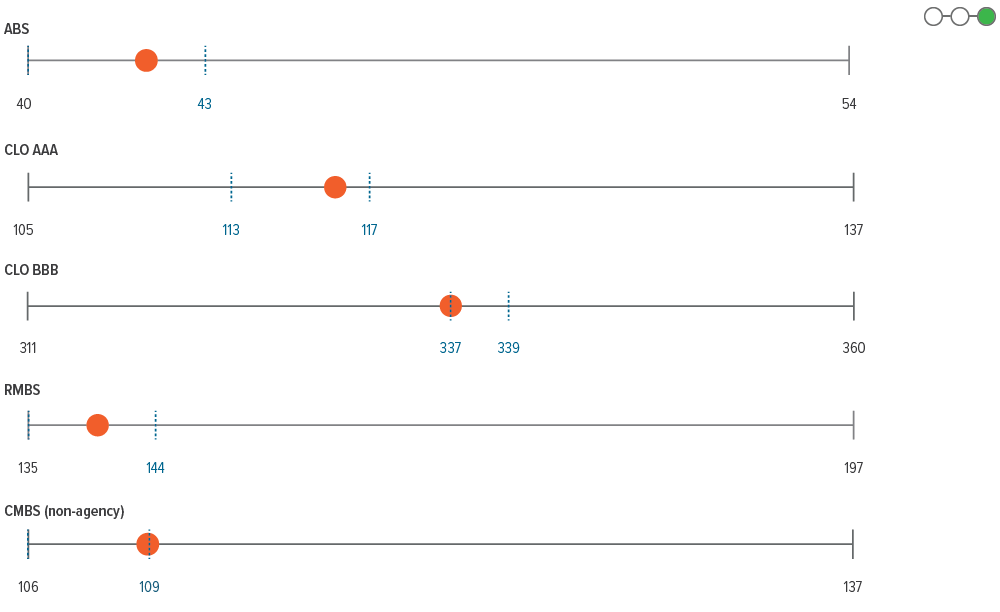

- Securitized credit remains the most differentiated opportunity set, but the outlook is uneven across subsectors: mortgage credit and CMBS look constructive, CLOs remain cautious, and consumer asset-backed securities (ABS) are more challenged.

- Mortgage credit benefits from strong housing collateral, accumulated home-price appreciation, and still-open investor allocations. However, higher rates can weaken some convexity benefits by reducing the likelihood that discounted mortgage bonds get paid back sooner through refinancing or turnover, which would otherwise help investors recover principal more quickly and reinvest at attractive yields.

- CMBS still offers selective spread premium as fundamentals improve and supply becomes more manageable, while CLO and ABS positioning should stay selective given AI, private credit, and consumer stress risks.

- Agency mortgage-backed security performance remains tied primarily to rate volatility, policy headlines, and technical flows rather than a deterioration in mortgage fundamentals.

- Suppressed prepayments and limited net supply remain supportive, while demand could improve on potential regulatory clarity and buying by government sponsored enterprises (GSEs).

- Near-term risks include disappointing GSE purchase execution, bank and overseas buyer hesitation, Fed reinvestment into Treasuries, and renewed rate volatility shocks.

- Emerging market hard currency debt has recovered with positive flows and tighter spreads, but high oil prices, geopolitical risk, and tighter financial conditions leave the macro backdrop fragile.

- Absolute yields remain attractive, but sovereign and corporate spreads are already close to historically tight levels, limiting valuation upside.

- Positioning should stay focused on higher-quality EM corporates and quasis, with caution on sovereigns, cyclicals, oil importers, and economies vulnerable to renewed stagflation pressure.