Fixed Income Perspectives: What Mixed Macro Signals Mean for Bond Portfolios

Head of Multi-Sector Fixed Income

It’s a familiar question in an unfamiliar setting: If inflation isn’t fully broken and growth isn’t overheating, how much risk should fixed income investors take— and where? Recent data complicate the outlook, but they don’t invalidate the case for balance and selectivity. Instead, they clarify where opportunities (and limits) are emerging.

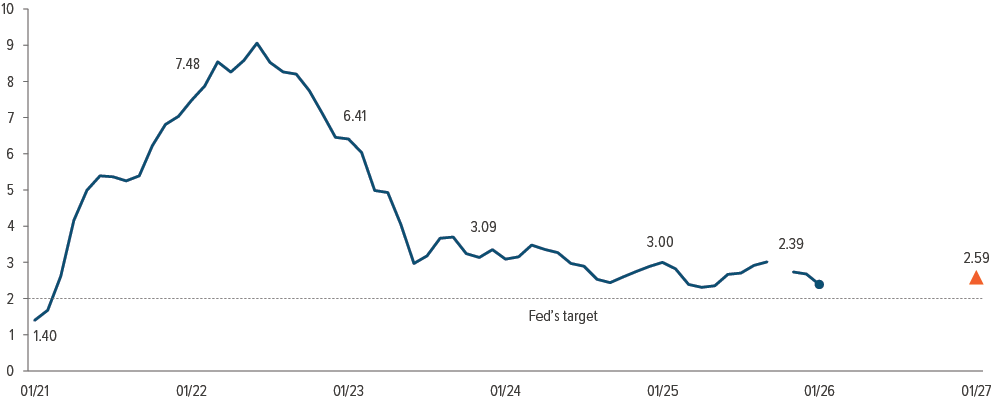

Inflation: Cooling, not cracking, despite rising dispersion

Recent inflation data have complicated the picture, but they haven’t reversed the broader trend. Inflation dispersion—where some categories see price increases while others don’t—has reached levels not seen in decades, pointing to an increasingly fragmented and less predictable environment.

Several recent factors could push inflation higher: Commodity prices have rallied, tax refunds this year may boost spending, and stricter immigration policies could tighten the labor market and wages. Additionally, while the Supreme Court recently struck down the use of tariffs under IEEPA, the administration has already turned to alternative ways to apply tariffs. These risks are real, but none are currently strong enough on their own to push inflation meaningfully higher (Exhibit 1).

As of 01/01/26. Source: Federal Reserve Bank of Cleveland. 2027 one-year estimated inflation.

Overall, demand is cooling, companies are finding it tougher to raise prices, labor markets are rebalancing, wage gains are normalizing, and shelter inflation is retreating.

What it means for portfolios

- Inflation risk hasn’t disappeared—but it’s increasingly uneven. Prioritizing sector allocation and security selection, as opposed to duration positioning, can help mitigate volatility.

- The case for aggressively positioning for higher inflation remains limited; while upside risks are present, the base case still calls for inflation to decline slowly, which favors high quality fixed income through elevated yields.

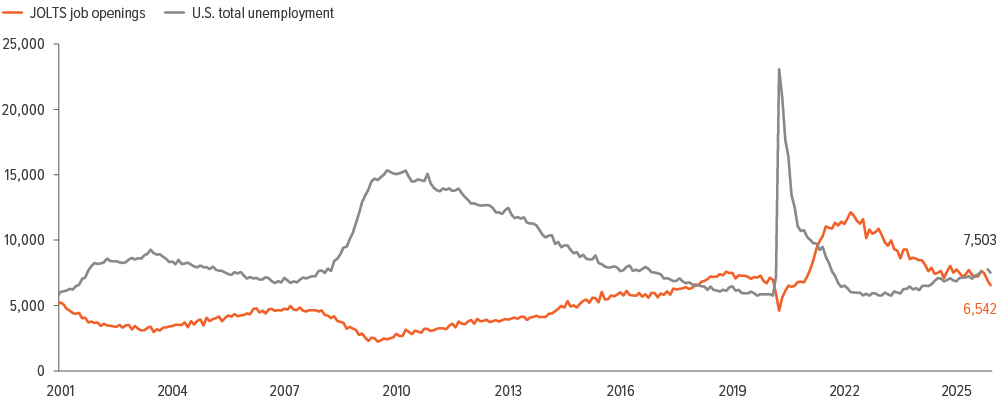

Growth: Steady momentum without excess

Growth tells a similar story. Economic momentum has improved as financial conditions ease and housing recovers, but the composition of growth matters. Consumer spending remains resilient even as income growth slows, with support coming more from borrowing than bigger paychecks. That dynamic is unlikely to last as long as in prior cycles. Financial regulations and households’ reduced appetite for leverage limit excess. Even so, overall demand has held up, with steady consumer spending driven largely by higher‑income households. This points to stability rather than exuberance.

Labor markets reinforce this view. Workers remain relatively scarce, helping to support wages, but cautious hiring suggests an economy that’s expanding without overheating.

As of 12/31/25. Source: Bureau of Labor Statistics, FRED.

What it means for portfolios

- Growth is supportive of credit, but not strong enough to justify indiscriminate risk taking.

- Credit selection matters more than market beta, as balance sheet strength—not demand acceleration— is driving stability.

Implications

- Duration: Volatile inflation signals argue for flexibility rather than conviction.

- Credit risk: Returns will be driven more by carry and selection than by spread compression.

- Sector allocation: Relative value and downside asymmetry matter more than broad exposure (see sector views below).

Sector outlooks

- 4Q25 earnings were strong as expected with fundamentals continuing to look supportive for IG spreads.

- Spreads remain tight, despite an expected heavy new issue calendar while higher yields supported demand for yield-based investors.

- We continue to keep IG risk low as spreads are back at historical tights, and prefer to take risk at the front end of the credit curve where exposure to spread volatility is lower.

- Valuation and lack of upside potential do not warrant large strategic weight, but with technical support and carry, we expect high yield to perform well in the near term.

- The magnitude of uncertainty in the market backdrop favors defensive business models and balance sheets, particularly at compressed spread levels.

- Technicals are supportive but softer than earlier in the year, with cash levels down and new issuance picking up.

- The overall carry of the senior loan sector should support performance on both a total return and excess return basis.

- After starting on a positive note, market conditions deteriorated sharply driven by a strong sell-off in the software space, which is among the largest sectors in the loan market.

- Longer term, supportive technicals, stable fundamentals, below-historical average payment defaults, and still-elevated yields that will continue to attract investors.

- The Administration’s announcement of GSE purchases sparked a sizable rally in spreads, however important details, including the timeline, remain outstanding.

- While follow through on purchases could provide additional support, spread levels are currently tight.

- Longer term, the fundamentals remain solid and the technical backdrop should smoothen out and benefit from lower rates.

- Securitized credit continues to offer attractive relative value in the current environment.

- Consumer-oriented ABS subsectors are balancing out among income cohorts, as labor market stability and tax refunds have the potential to provided much needed support to lower income consumers.

- CMBS fundamentals remain supported by stable property performance and continued deal flow. That said, there are still a handful of deals that will remain under stress, and will likely hit headlines later in the year.

- Even with heavy issuance in non-agency RMBS, deals cleared with minimal slippage. Market remains “dialed in”.

- Relative valuation is weaker and some credit concerns have re-emerged in CLOs, making the tailwinds less strong. We remain positive, but with lower conviction.

- In hard currency, spreads are at historically tight levels, while local currency appears more attractive due to elevated real yields in certain countries.

- Resilient U.S. growth and above target inflation should sustain attractive yield levels for hard currency assets.

- A weaker U.S. dollar should support continued inflows in EM assets, particularly higher yielding local bonds.