Senior Loan Talking Points - April 30, 2026

Managing Director, Head of Bank Loans and Global CLOs

Weekly Notables

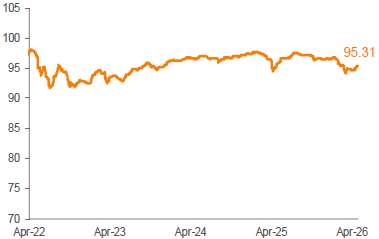

Risk assets maintained their recent momentum, with equities delivering another week of strong gains and credit spreads tightening further. Although oil prices and Treasury yields both edged higher amid continued uncertainty surrounding the Iran conflict, these concerns were offset by strong corporate earnings and stable economic data prints. As expected, the Fed left interest rates unchanged at this week’s FOMC meeting, but there was more dissent than usual among members, with the committee moving from an easing bias to a more neutral stance. Fed funds futures continue to price in zero rate cuts in 2026, which is supportive of a strong carry environment in loans. The Morningstar LSTA U.S. Leveraged Loan Index (Index) returned 0.13% for the seven-day period ending April 30. Coupon income drove performance this week, as the weighted average Index bid price moved just one basis point higher, to 95.31.

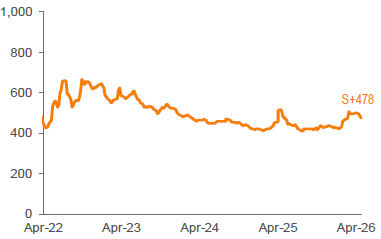

The primary market experienced an uptick in activity this week, although much of the increase was attributable to repricings and amend-to-extend transactions. Away from these deals, new-issue supply remained subdued at just $5.4 billion. April’s issuance volume totaled $14.8 billion, the lowest monthly figure since last April at the height of the tariff-related volatility. In the forward calendar, repayments now outstrip supply by $11.6 billion, compared to net repayments of $4.7 billion last week.

Secondary trading levels were stable this week. Positive earnings and strong demand from ramping CLOs are providing strong bid support, with stable and higher-quality credits remaining in high demand in the absence of a deep new issue pipeline. The percentage of loans trading above par continues to increase and is now tracking 38.9% compared to the lows of 9.3% seen in March before the loan market resumed this latest ongoing rally. There’s increased market chatter whether the continued rally in loan prices ushers in a new repricing wave given the strong technicals. Earnings news were front and center, as a handful of issuers reported quarterly results with generally positive trends providing continued tailwinds. Performance across ratings reflected an up-in-quality bias among investors, with CCCs trailing higher-rated credits after a few weeks of outperformance.

CLO managers priced four new deals this week, bringing YTD issuance to $54.6 billion. The recent tightening in the liability stack and the decline in the overall cost of capital have resulted in a resurgence in CLO issuance volume. It’s likely that this momentum will continue into the coming weeks based on the volume of deals that have been announced and are currently being marketed. US retail loan funds experienced a modest net inflow of $14 million for the week ending April 29, according to Lipper.

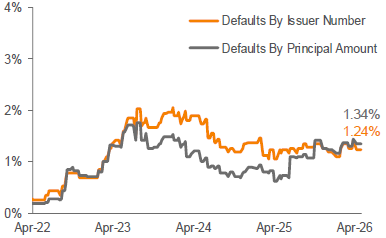

There were no payment defaults in the Index this week.

Source: Pitchbook Data, Inc./LCD, Morningstar LSTA US Leveraged Loan Index. Additional footnotes and disclosures on back page. Past performance is no guarantee of future results. Investors cannot invest directly in the Index. *The Index’s average nominal spread calculation includes the benefit of base rate floors (where applicable).